Introduction

The role of the state in the delivery of public goods and its relationship to the voluntary sector providers of these goods is continuously evolving in Canada, as elsewhere. Throughout the 1980s and 1990s under the rise of neo-liberal strategies including New Public Management, the delivery of public goods was increasingly contracted out to non-state actors in an attempt to promote market-based tools and results-based management, and to reduce the size of the state. Not only did contracting out replace public sector provision of public goods and competitive tendering supersede preferences given to nonprofits, but the means of supporting voluntary organizations and building capacity in this sector was also placed on a competitive footing. Relatively unconditional grants that provided support for the operations of many voluntary organizations were abandoned in favour of project funding that is awarded on a competitive basis and subject to the terms of ‘contribution agreements.’ In effect, because the contribution agreements that govern project-based funding come with pre-specified terms and conditions and deliverables that are largely under the control of government, they are barely distinguishable from fee-for-service contracts.

A defining feature of a contract is the nature of accountability associated with it. Because contracting out vests “substantial discretionary authority in entities other than those with ultimate responsibility for the results,”1 the main function of the legal mechanism of the contract is to allow the principal (government) to exercise control over the performance and the products of the agent (the voluntary organization) and to provide public assurances that public money has been spent appropriately. This could be described as ‘vertical’ accountability in which subordinates or contractors are expected to comply with standards set by superiors or principals.2 When the primary goal of contracting out is to ensure the efficient delivery of public goods according to pre-set standards and conditions, accountability mechanisms can be expected to achieve control and assurance rather than facilitate learning or performance improvement.3

Project-based funding has another purpose besides mere purchase of services, however. A related, indeed often primary, goal of such funding is to enhance community capacity and encourage the development of best practices and innovation by voluntary organizations.4 In this sense, project funding is part of the broader reconfiguration of relationships between government and the voluntary sector that is implied in the transition from New Public Management to a ‘governance’ paradigm that emphasizes collaborative partnerships involving the sharing of power, risk, responsibility, and decision-making; that works through networks rather than hierarchies; and that makes use of a wide variety of policy tools.5 Effecting this transition to a more collaborative or distributed model of governance rests on constructive relationships with non-governmental partners, including articulation of mutual responsibilities. In this context, a ‘horizontal’ dimension of accountability —the dual accountability of government and its partners as co-producers of policy and of services and the accountability of each to citizens and users—becomes equally important to more traditional vertical lines of control and authority.6

By relying on project funding as the main basis of support for capacity building in the voluntary sector and by treating such funding as essentially contracts with tight top-down controls, the exigencies of vertical accountability are crowding out and, in fact, hindering opportunities to establish the mechanisms of horizontal accountability that are needed in a model of distributed ‘governance.’ This article examines both the vertical accountability (to government for the federal mandate) and horizontal accountability (of partners to each other and to their users and stakeholders) of project funding by the Government of Canada. Based on 29 interviews with representatives of voluntary organizations that have been in receipt of project funding both preand post-2000 when the federal accountability requirements became much more stringent, we show how project funding promotes accountability to government largely at the expense of accountability to partners and their users and stakeholders. Moreover, even the effects of vertical accountability requirements are limited: with an emphasis on financial reporting, they do little to enhance accountability for results. The effects of the efforts to strengthen accountability in recent years has led to a situation in which too much accountability may mean too little. The funding tool is unable to nurture meaningful accountability and also produces detrimental impacts for voluntary organizations. The result, we suggest, is analogous to fitting a square peg in a round hole. If the federal government is to contribute to capacity building and innovation in the voluntary sector and to build a more constructive, collaborative relationship with the sector over the long run, new funding tools that are less restrictive than the contract-like contribution agreement are needed to better fit the shape of this new hole. In the conclusion to this article, we discuss how such a tool might be designed to nurture more meaningful accountability, both vertically and horizontally.

Contracting as a Policy Tool

As a policy instrument, a contract can be thought of as a means of defining the relationship and aligning the interests of government as a principal and the provider/purchaser of services with those of a third party agent as the producer of those services, thereby avoiding issues of moral hazard.7 More precisely, a contract is a reciprocal, legally binding transaction between (at least) two parties that involves mutual benefit and detriment regarding specific tasks, products or services.8 The most important aspect to note about the purchase—of-service contracting tool is the government’s ability to exert control by setting the terms, conditions, and deliverables.9

Like all policy instruments, contracting is used to address a particular set of governmental and policy problems under certain economic, social, and political conditions.10 With the rise of contracting and project funding in the 1980s and 1990s, these problems were defined mainly in terms of economy and efficiency. The concern with reducing the costs of government was one impetus to contracting out public services and to cutting the long-standing granting programs that provided support for the core operations of many voluntary organizations. Equally important, however, was the concern by the populist right in Canada that government should not fund organizations engaged in advocacy, particularly those critical of government.11 Where funding continued to be provided, it came mainly in the form of contribution agreements that maintained control and efficiency through a competitive process. These agreements are conditional transfers “made when there is or may be a need to ensure that payments have been used in accordance with legislative or program requirements. More specifically, contributions are based on reimbursing a recipient for specific expenditures according to the terms and conditions set out in the contribution agreement and signed by the respective parties.”12

Contribution agreements that are the basis for providing support to the voluntary sector and contracts that govern the purchase of services thus converged as policy instruments.

The result has been a blurring and, indeed, a confusion of funding goals and funding styles. A recent study prepared for the Baring Foundation in the UK distinguishes three distinct funding styles: giving (providing unconditional support); shopping (procuring quality, often standardized, services in a marketplace); and investing (building capacity for longer term returns).13 While the intent of some project funding, secured through contribution agreements or contracts, is a form of procurement or shopping, others are really investment in longer term capacity. Yet the use of a contract-like funding instrument as the basis for both shopping and investment seldom enables government to obtain higher quality products, to expand the ‘marketplace,’ or to contribute to the longer term sustainability and innovative capacity of the service producers. As the Baring Foundation study concludes, governments and other funding organizations “that wish to ‘shop’ from well managed, high performing, innovative organisations need to attend to their relationships with these suppliers, and do so in a way that builds capacity rather than preventing it.”14 If investment is the real goal, however, capacity and innovation can seldom be realized through competitive contracting; rather, a much broader range of funding instruments is required. With new instruments comes a rethinking of accountability.

The Accountability Dimensions

Accountability is generally seen to encompass two related but different concepts: answerability and responsibility.15 First, accountability includes the answerability or the reporting requirement of actors involved in producing and delivering public goods. As Gregory notes, “accountability, as the word itself suggests, is about the need to give an account of one’s actions…[since] managers must know what their subordinates are doing, and their subordinates must tell them…[otherwise] work that is hidden is potentially threatening to the organization.”16 Answerability could, mistakenly, be seen to be a neutral, technical, and clear-cut process. As Day and Klein note, it is a value-laden process as it involves determining how objectives and performance are defined, and by whom, in the first instance.17

Whereas answerability demands the expression of actions to others, responsibility concerns the acceptance for actions.18 It involves both ‘being held to account’ via sanctions or other methods of redress and ‘taking account’ of stakeholders’ needs and views in the first place and responding to these by revising practices and enhancing performance as necessary.19 Responsibility “is to be understood not as a formal, externally imposed duty but as a felt sense of obligation. It is not only ‘upward-looking’, in a hierarchical sense, but may be experienced as a pull in other directions to a number of ‘significant others’.”20 Following Gregory’s interpretation of responsibility, we suggest this necessarily includes the demonstration that the goals outlined in a contractual relationship were the right goals in the first place and that there is acceptance for fixing what has gone awry coupled with continuous learning.

The functions of accountability are thus three-fold, according to Aucoin and Heintzman: accountability as control, assurance, and learning.21 Accountability as control attempts to ensure contracts control the use of public funds whereas accountability as assurance seeks to assure all vested stakeholders that the rules of the contract have been adhered by third parties. To date, the accountability regime associated with voluntary sector contracts has largely been aimed at control and assurance. Contracts do not, however, necessarily exclude the third function of learning as a means for continuous improvement of management and operations.

Vertical Accountability

Giving an account of and taking responsibility for addressing problems created or not solved could be seen to operate in both vertical and horizontal directions. Within government, vertical accountability reflects the doctrine of ministerial responsibility as a central feature of Canada’s Westminster parliamentary government: public servants are accountable to their superiors who are accountable to their superiors and so on, thereby effectively structuring accountability to flow in a vertical manner upwards toward the minister and Parliament.22 In each of these superior-subordinate relationships, Aucoin and Jarvis note, “the degree of accountability depends upon the extent to which authority has been delegated, formally or informally, for general or particular responsibilities.”23 In purchasing arrangements with voluntary organizations, government uses contracts or contribution agreements to achieve this type of vertical accountability.

As the principal in project funding, government sets the accountability requirements that voluntary organizations must satisfy. These accountability requirements have tightened up following the so-called scandal at Human Resource Development Canada (HRDC) that began in January 2000 with the release of an internal audit of HRDC’s grants and contributions programs. This internal audit concluded that the grants and contributions programs contained inadequate documentation and missing information. While not a financial audit, the media portrayed it as such, implying the programs had lost a billion dollars of taxpayers’ money. While the media represented this as a ‘scandal’ to Canadians, more analytical reviews cast doubt on whether there was any mismanagement of taxpayers’ dollars at all or at least suggested that the scope of any such mismanagement was overblown.24 Regardless of whether a real scandal had occurred or not, the response from the government was definitive: a bureaucratization of the funding process with tighter accountability requirements than ever before. This stringency included new rules from the Treasury Board Secretariat supplemented by new rules instituted by funding departments. The new departmental rules are not all exactly the same but they all worked to significantly tighten up accountability requirements.

These requirements are onerous, at both the front end of seeking approval for funding and on the reporting and audit ends. Applying for a contribution agreement now involves a completed application form with detailed background information on the organization and a complete proposal with concrete deliverables and outcomes, all of which must be approved by various levels within the department. As the application moves through the process, it is not uncommon for nonprofits to have to re-write the application several times. Once the agreement is approved, the monitoring procedures require the submission of quarterly cash-flow statements and other reporting requirements.

For applications to Social Development Partnerships Program of Social Development Canada, for example, the verification of a claim includes an 11-point checklist while a “variance of 15% from predicted cash flow during a reporting period (which could be as short as a month) may trigger a contract amendment process that involves a 17-point checklist.”25 The review of an agreement consists of four forms and 22 checkpoints in addition to an Activity Monitoring Report.

Born out of crisis, the major goal of these requirements on contributions was to ensure that accountability controls were in place—and seen publicly to be so—rather than to carefully balance any adverse impacts on the contracting organizations.26 The underlying implied premise is that, as contractors, voluntary organizations are not to be trusted; rather, government must exercise tight control over what kinds of objectives and projects are approved and must monitor and audit on a micro scale. As we will see, the impact has been enormous transaction costs for voluntary organizations (and, undoubtedly, for government) and an erosion of trust.

Horizontal Accountability

Vertical accountability, considered the traditional model of accountability and usually expressed through financial control, has come under strain in recent years.27 Prior to the introduction of New Public Management, government largely responded to public policy problems independently of other societal actors so the vertical accountability structures, designed by government for governmental activity, were sufficient. The incorporation of non-governmental actors charged with delivering public goods, however, introduces challenges to this traditional model of accountability as the responsibilities of government and non-government actors have become blurred.28 The fact that accountability has become increasingly complex with the advent of New Public Management is noted by Mark Considine:

We therefore need to approach the accountability issue as a problem with multiple levels and more than one possible meaning, Of course, this has always been the case to some extent. Public servants managing large programs have often had to balance demands for accountability from their executive branch, from congressional committees, from ministers outside their portfolio and from different organizations representing parts of the citizenry. However, until recently these pressures were generally defined within the remit of a single public ministry or agency. With the advent of entrepreneurial government and the enterprising state, expressed most obviously in extensive forms of contracting out, these organizational boundaries and identities are less able to contain or limit the accountability issue.29

While New Public Management has challenged the vertical accountabilities of the state, the transition in governing from New Public Management toward governance generates a new dimension of accountability for consideration. With its emphasis on collaborative partnerships, governance promotes horizontal accountability among actors involved in the provision of public goods. Aucoin and Jarvis note that, “since the parties involved shared authority and responsibility, they may consider themselves accountable to one another for the discharge of their respective responsibilities in the collaborative undertaking. In this sense, they may speak of a ‘horizontal’ (equal-to-equal) as opposed to a ‘vertical’ (superior to subordinate or principal to agent) accountability relationship.”30

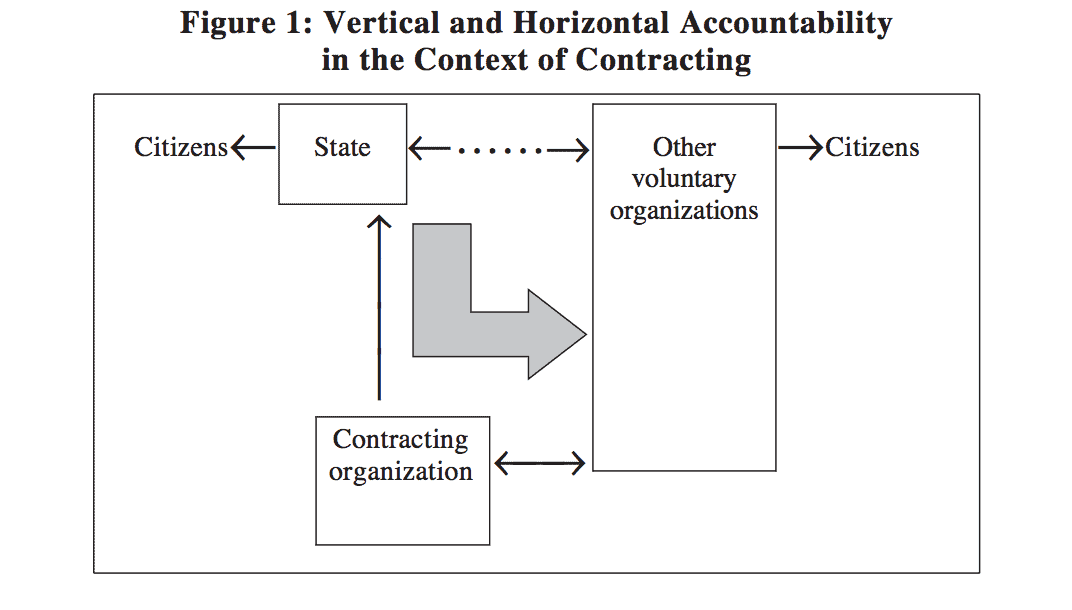

Figure 1: Vertical and Horizontal Accountability in the Context of Contracting

Governance suggests that partners are horizontally accountable to each other with each partner also required to “respect their own vertical accountability to their respective bodies corporate.”31 This idea of horizontal accountability within governance is illustrated by the dashed arrow in Figure 1. Horizontal accountability does not replace vertical accountability—it merely adds to the accountability requirements of partners. The resulting implication is that all partners must contribute to horizontal accountability while simultaneously contributing to its own vertical accountability.

Even when the partner is a contracting organization, horizontal accountability still flows from vertical accountability. The block arrow diagrammed in Figure 1 illustrates that through the vertical contracting relationship emerges horizontal accountability as well. The contracting organization must account for its actions in a vertical manner to government, but the horizontal accountability of the contracting organization to the rest of the voluntary sector may be both directly and indirectly affected by this. No voluntary organization, even when involved in a contractual relationship with the state, is wholly isolated from the rest of the sector or from its members and users.32 The organizations that make up the sector weave numerous inter-connected networks with their multiple crosscutting funders, members, stakeholders, users, and community members. Underpinning these close relationships between voluntary organizations is trust—the belief that the other voluntary organizations are doing their part, through self-governing, to contribute to the development of the sector and its overall credibility.33

Impact on Vertical Accountability

To assess how the contribution agreements associated with project funding promote both vertical and horizontal accountabilities, in-person and telephone interviews were conducted with 29 nonprofit organizations that have received project funding in the past several years from either the Social Development Program of the then HRDC or the Multiculturalism, Official Languages Program of Canadian Heritage. Additionally, seven interviews were conducted with civil servants and leaders in the voluntary sector.34

These interviews reveal just how significant the effects of the tightened accountability measures for contributions since 2000 have been. Contributions now require much more detailed reporting and review of projects to demonstrate that the contract requirements have been satisfied. This particular form of accountability is quite narrow and is focussed on reporting relative to the terms of the contract, not on whether the overall goals of the program were appropriate or on performance assessment more broadly. As one respondent noted, “The process has become more bureaucratic, detailed, and diligent. Accountability is essential, but this process does not build accountability since it focuses only on the financial aspect and does not incorporate other important elements including impacts on society.”

While the contributions now demand detailed reporting and review requirements, this appears to have produced a scenario whereby too much accountability actually means very little accountability. With its emphasis on the minor details associated with reporting and reviewing, this funding instrument forces the recipients of the contract to make estimated guesses about expenditures that are often incorrect and does not contribute to meaningful accountability. One respondent indicated that she previously could include a 10% ‘administration fee’ to pay for core operations, including rent, photocopier, etc., on the application form. The funding department no longer accepts this; it now asks extremely detailed questions such as, “How many photocopies will be needed to complete this project?” She must break down this ‘administration fee’ into minute components, which becomes a guessing game because she cannot predict how many photocopies will be needed for the project.

Another issue that contributes to too much accountability resulting in little accountability is the lack of transparency and cross-subsidization of philanthropic money used to pay for public goods. With heightened accountability requirements, new layers of review that involve greater scrutiny produce delays in the approval process for funding. It is not uncommon to wait up to 8–12 months for approval. According to respondents, this makes it difficult for them to strategize effectively. One respondent shared this example: His organization hired a staff person on a limited-term appointment to coordinate its annual special event. This person is normally hired in the fall, six months before the event, which is held in the spring. However, because of delays in the approval process, this organization did not receive approval until one month before the start of the special event, and the funding department does not allow organizations to backdate expenses they incurred in the fall. The organization was faced with a difficult choice: take a risk and hire the person to start the work in the fall and hope for funding or wait until the funding comes through one month before the start of the special event and then hire the person. The latter choice would have placed the entire project at risk because the bulk of the work needed to be completed over the fall and winter months. Opting for the former, the organization proceeded with the project and hired a staff person in the hope that the funding would come through at a later point. It had to use funds from other sources to cover the expenses until the funding came through—a situation that is very common and is often referred to as “stealing from Peter to pay Paul.” When the funding finally comes through for this project, it is used for another project that is waiting for funding, so the funding machinery becomes a patchwork quilt.

Fortunately for this organization, it has a relatively large quilt with many patches. It is able to survive even though it is not practicing full due diligence because the funding from the contracts and projects is not used solely for the purposes intended. The current accountability regime governing public project funding poses even harder choices for small organizations.35 In effect, vertical accountability and horizontal accountability are both jeopardized by the use of private money to subsidize public services and projects.

Impact on Horizontal Accountability

Voluntary organizations are self-governing entities with a responsibility to users, stakeholders, and the broader communities they serve.36 The heightened accountability requirements of governmental contracting have several effects that are both significant and negative for voluntary organizations that rely on this form of funding and that make it difficult for these organizations to be accountable to their various constituencies.

One effect cited by many interviewees was mission drift. This occurs when a nonprofit chases funding dollars that may not necessarily reflect its overall mission so that the ‘[funding] tail starts wagging the dog’. Consider the example of one local voluntary organization in our study. This organization, which is dedicated to assisting low-income families, applied for project funding to initiate child-care programs for new immigrant women. The funding department refused to fund such a program but indicated that it would provide funding to initiate a soccer club for youth, despite the fact that numerous such programs already existed in the community. In an attempt to secure funding that would allow it to remain open, the nonprofit initiated soccer clubs instead of the child-care program even though the child-care program truly reflected its overall mission and was identified as a pressing need by the community. This top-down approach negates the benefit of the nonprofit sector—its ability to identify needs in the community—and encourages mission drift.

Mission drift can also occur in other ways. Interviewees repeatedly said that the detailed reporting and review mechanisms take staff and volunteers away from working on the front-line with their users, members, or communities. The contributions do not allow for funding of administrative infrastructure, and few contracts cover the administrative costs of preparing, executing and reviewing a contract. As such, staff and volunteers, already in short supply in many voluntary organizations, are stretched even further and, in completing the increased requirements of the contract, effectively are lost to their programs and communities. This added administrative pressure of the contracting tool contributes to the ‘burn-out’ felt by staff and volunteers, many of whom began working for the organization in the first place to help people, not to become involved in administrative reporting. This is not to suggest that nonprofits do not want to be held accountable to government; they do, but funding tools need to acknowledge the capacity and means of voluntary organizations to do so effectively.

Not only do delays in the approval process reduce transparency and the overall accountability for the federal mandate, but they also affect nonprofit organizations. Some nonprofits rely heavily on government funding for their overall budget; delays can threaten the survival of some of these organizations. One provincial umbrella organization we interviewed noted that it did not have funding for nine months due to time delays in approving a contribution agreement. The application went across five different government desks for approval, and throughout the process the organization was asked to re-write the application several times. To survive the nine-month funding gap, the sole staff person volunteered her time (some 400 hours) to help the organization maintain its office space, which was donated by the landlord. Despite these attempts to buffer the instability of funding, some programs were eventually lost and the organization suffered a loss of credibility, which, in an era of networks, trust, and reputation, is an important form of capital.

Respondents observed that the project-funding tool also deters innovation and creative problem solving. The sector is well known for its creativity when responding to public policy concerns, but current funding practices favour more conservative, less risky projects. The accountability regime associated with this type of funding encourages control and assurance through required deliverables and anticipated outcomes that must be outlined in advance. Generating deliverables and anticipating outcomes for new creative approaches to public policy concerns (especially preventative programs) is a difficult task, however. Further exacerbating this is the requirement that all projects must be ‘new’, thereby hurting ‘existing’ programs and projects that have been shown to work well. Besides deterring innovation from the outset by at least implicitly favouring more conventional, less risky projects, the tool also hinders the sharing of innovative learning once funding has been granted to a project. Respondents noted that an audit of the funded project might not pass if an innovative aspect appears in the audit but was not included in the original funding application. Where learning has occurred in the context of problem solving during the course of a project, it is often disguised rather than shared.

In sum, the project-funding tool demands a significant amount of reporting from the contracting organization. However, this onerous reporting focuses mainly on financial reporting, which aims only at satisfying the ‘answerability’ portion of accountability and then mainly for expenditures not results. From the accounts of the voluntary organizations we interviewed, it appears that the project-funding tool promotes mission drift, jeopardizes programs and organizations with its time delays, and hinders innovation. Moreover, the fact that nonprofits must privately subsidize public sector projects is an accountability issue in its own right, but one that is invisible in current debates on accountability. Networks may be altered and weakened by project funding, which reinforces regular rounds of competition among nonprofits, absorbs significant resources for stringent reporting, and reduces capacity for network building.37

The cumulative impacts of this funding tool translate into reduced capacity for nonprofits while hurting their credibility and jeopardizing their ability to cultivate community relationships, promote public deliberation, encourage innovation, and contribute to governance.38

Toward Smart Funding and Accountability

The existing contract-like basis for project funding is not achieving effective accountability in a vertical sense and is actively hurting relationships and horizontal accountability. Moreover, the environment in which project-based funding was developed has changed significantly as the approach to governing has shifted attention from the market-based efficiencies and cost containment of neo-liberalism to the need on the part of governments to work in more collaborative ways and to foster active citizenship, including strengthening the voluntary associations that contribute to citizenship.39 As the governance environment evolves, so too must funding and contracting tools, particularly those that have a primary or secondary purpose of building capacity in the voluntary sector, rather than simply shopping for goods or services.

Leaders from Canada’s voluntary sector have made the case strongly to government that the current contracting and accountability regime is not sustainable. As Jean Christie from the Voluntary Sector Forum noted in the consultations on the 2005 budget:

To put it bluntly, organizations across Canada are buckling under the pressures of short-term funding and of project funding. They’re swamped by the paperwork they have to do for their funders, and they’re spending very scarce resources to do that paperwork. This problem has now been very well documented… We would like the Government of Canada to take leadership on this issue and to find ways to streamline funding processes and accountability requirements across the federal government and to address the problem more widely with other funders. Let me say very clearly here that we’re not talking about more funding at this stage; we are talking about better funding, more strategic funding. Let me also say that we are not talking here about abdicating our responsibility to account for public funds. Organizations that receive public funds know we have a responsibility to do that. In short, what we’re asking for is what we call smarter funding and more appropriate accountability, consistent with the code of good practice on funding that both the government and the sector have signed.40

Governments in other countries have begun to take leadership toward smarter funding and contract relationships for voluntary organizations as part of the post-New Public Management wave of public sector reform. One approach, used in Wales and Quebec for example, has been to continue (or reinvest in) core operational funding as well as extending the terms of such funding to provide greater stability and capacity.41 Another major route is to move in the direction of relational contracting, as is being explored in New Zealand, Australia, the UK, and elsewhere.42 Although in comparison to most other democratic countries, Canada provides minimal funding to national infrastructure organizations in the voluntary sector, we will focus on the latter as a model for moving toward smarter funding, given that the federal government appears to be reluctant to entertain in any serious way the idea of expanded operational funding.

Relational contracting rests on a basis of trust and a commitment to common goals.43 Although it can maintain a legal core, it emphasizes a long-term relationship rather than a one-off exchange and a specification process. This approach assumes that each party is motivated to maintain its credibility and reputation with the other, and it thus depends more on open communication and processes than on rules and more on maintaining flexibility than on pre-specifying detailed requirements.44 If one were to think of a continuum anchored at one end by the traditional, discrete, rules-based contract and at the other by the relational contract, as one moves from the former to the latter, the emphasis shifts, suggests Boyle, “from detailed contract specification to statements of the process to be followed when adjusting the contract: rules determining the length of the relationship, rules determining the response to unexpected factors that arise in the course of the contract, and rules concerning the termination of the relationship.”45

The advantages of relational contracting between governments and voluntary organizations is that it builds stronger, trust-based relationships, reduces transaction costs, provides greater flexibility in being able to respond to new needs or demands, and offers greater scope to solve problems as they arise during the course of the contract.46 By putting the emphasis on mutually agreed-upon results-based measures as the standard of performance assessment rather than on minute financial reporting as currently exists in Canadian contributions, such contracts can still maintain appropriate vertical accountability. Evidence from New Zealand suggests that where such contracts have a distinct advantage is in promoting greater horizontal accountability by fostering greater coordination and collaboration among contracting agencies and by motivating them to pool resources and create synergies.47 Relationship contracting has been used most effectively in contracting by local authorities where the players are already well known to each other, or where there are relatively few potential contractors available, or in certain human services in which it would be detrimental to change contractors on a regular basis.48

The main disadvantages are twofold. First, relational contracting involves selecting certain voluntary organizations for longer term relationships and could thus be seen to create insiders and outsiders. For funding programs at the federal level aimed at building capacity among the national infrastructure organizations, the size of the pool is quite small so that concerns over creating a two-tier system can be averted. Second, in the current accountabilityobsessed political environment following the federal sponsorship scandal and the resulting Gomery Inquiry, making a case for reducing reporting requirements is a hard sell for the public service. That said, given the evidence which clearly indicates that the existing method of project funding is unsustainable49 and that the current accountability regime is both incredibly onerous and not an effective means of promoting performance improvement, a case for change does need to be made.

The impact of the accountability requirements related to contributions that we have described does not come as news to the federal government. The need to consider options for more strategic funding began to be considered with the creation in 2005 of a Task Force on Funding Instruments. We argue that the principles, if not the full blown model, of relational contracting could serve as a useful basis for advancing the development and implementation of ‘smart accountability’ as part of this work. By looking to the principles of relational contracting, the federal government could both meet its own existing policies50 and adhere to the Code of Good Practice on Funding that was agreed to under the Government of Canada-Voluntary Sector Accord signed in December 2001.51

The first step in this direction, as long advocated by the voluntary sector and as outlined in the Funding Code, is to move to longer term, multi-year funding horizons. Greater flexibility to carry over funding not spent in a particular fiscal year to the next would allow experimental or innovative projects to be more results-driven than rule-driven.

A second step is to drop the fiction that government is always shopping for something new from providers of which it knows nothing, thereby requiring voluntary organizations to describe and justify themselves and their projects anew for each and every application. Relationships exist, and they matter. In some cases, there may be only a couple of voluntary sector organizations capable of providing the service, particularly if these organizations are already the only providers, so a full blown competitive process is a waste of both time and money. One way to avoid unnecessary background checking on applicants for each round of funding is to adopt the concept of ‘passporting’ that is used in the UK.52 Passporting can occur in two ways. In situations where organizations must apply to more than one federal government funder for the same project, the passporting principle allows for sharing of information about the applicants among the funders, thus reducing the burden of multiple applications. Where voluntary organizations repeatedly seek funding from the same department, passporting allows organizations with long-standing relationships and a good track record with the department to bypass certain elements of information provision and background checking. This should have the beneficial effect of speeding up the approvals process, although other measures, such as giving more autonomy to local/regional offices, may also be needed to promote timely approval of projects.

To ensure that the process is not a closed loop whereby only previously funded organizations are considered for future funding, the introduction of a communitybased funding model could be helpful. Separate application processes for national infrastructure organizations and more place-based initiatives for local/ regional organizations would facilitate support for community service providers and investment in supporting the broader infrastructure of the voluntary sector.

The third step is to shift the basis of accountability from detailed reporting on inputs (mainly reporting on financial expenditures) to a focus on outputs and results.53 For all the discussion of results-based management in government, there is, in fact, little management to results in the project funding realm. Because the real goal of project funding is often investment in the provider rather than procurement of standardized services, it would be vital as part of a reorientation to results through relational contracting to develop mutually agreed upon outcomes and parameters at the beginning of a funding agreement. In addition, it is important to allow the contracting organization some scope to undertake creative problem solving during the course of the project. This means that actual activities might deviate somewhat from the original plan. This step also entails a change in the audit culture and attitude from micromanaging small details to collaborating on making projects effective. Sound risk management would imply monitoring high-risk projects more closely but auditing and intruding on the rest more lightly. For projects below a certain threshold, say $100,000, the project officer might be allowed more flexibility to make decisions on oversight.

A shift to a more performance-driven model of funding and accountability necessarily involves a change in the role and relationship of departmental program/project officers with the organizations they fund. In the current system, program officers function mainly as auditors and police officers. Funding instruments that can truly enable government to determine where to make wise investments in voluntary sector infrastructure mean a return to the role of program officers as nurturing and enhancing the performance of programs by building relationships with the organizations they fund.54 Improved and coordinated training for project officers is needed on issues related not only to accountability, but also to partnership building and knowledge of the voluntary sector more generally. A key to developing trust-based relationships will be to find ways to keep these officers, often quite junior in rank, in their positions for longer periods of time so that they can develop solid working relationships with their constituencies. Due to the high mobility within the public service at the present time, program officers no sooner develop some knowledge of the organizations their programs fund than they move on to other jobs.

Finally, a focus on performance improvement and learning could be made more effective by providing better ways for organizations to learn from each other. For example, a department could convene the voluntary organizations it has funded each year to share information about good practices related to performance assessment.

What would it take to facilitate a new and improved funding process for Canada’s voluntary organizations? The policy on transfer payments from the Treasury Board Secretariat provides room for some flexibility with regard to this funding instrument, although some adjustments may be necessary to fully apply the principles we identified to a new funding instrument. The interpretation of the Treasury Board’s policy by some federal government departments, however, is sometimes more restrictive, so departments will need to change their own practices. But more than existing mechanisms and accountability regimes are clearly needed. By supporting the work of the Task Force on Funding Instruments, the federal government may be able to develop some truly innovative new mechanisms that are better suited to both shopping and investment.

Ultimately, what is really required is a culture change regarding accountability and how it intersects with the funding of voluntary organizations. This entails engaging in a public debate on accountability by moving beyond the myth that the problem is too little accountability. Rather, the debate needs to face the high transaction costs and the limited ability of the current regime to promote results-based performance assessment or performance learning. Such a change, however, may be difficult to achieve given the zeal for accountability in light of the Gomery Inquiry.

Conclusion

The contract in Canada, once primarily used as a management tool to control performance, is now a governance tool used to guide the relationship between the federal government and the voluntary sector. The accountability regime associated with project funding, however, has significant and largely negative impacts on voluntary organizations as they deliver public goods to Canadians. This threatens not only service delivery but the internal self-governance capabilities of the organizations themselves. This accountability regime clearly favours vertical accountability largely at the expense of horizontal accountability to governance partners. But even with an increased emphasis on securing vertical accountability, the regime has produced a scenario in which too much accountability actually results in very little meaningful vertical accountability. The changes to the accountability regime in the post-HRDC scandal have focused more on demonstrating that the requirements of the contract were met than on asking whether the goals outlined in the contract were indeed the right ones in the first place. This may reinforce answerability, but it undermines the responsibility aspect of accountability.

In light of these negative impacts, we argue that a new funding tool is needed if the relationship between the federal government and the voluntary sector is to flourish in years to come. The concept of relational contracting articulates some of the principles that could guide the development of new funding instruments. The task is not merely a technical one of redesigning contracting tools, however. It is one of sorting out the current confusion over the goals of funding mechanisms for voluntary organizations. Those instruments that enable governments to shop well and procure quality services may be ill-designed to allow them to invest in the voluntary sector.

The federal government has begun a challenging but important task in exploring possibilities for new funding instruments. There is much to be done and it remains to be seen whether contribution agreements and contracts can be modified to adequately promote vertical and horizontal accountability for both government and voluntary organizations or whether entirely new funding tools and accountability measures will be required. Either way, the design of new or modified ‘pegs’ is desperately needed to allow for more meaningful forms of accountability and to enable governments to both fund services produced by the voluntary sector and to invest in the sector for its long-term viability and contributions to our society, economy, and governance.

NOTES

1. Lester M. Salamon, “The New Governance and the Tools of Public Action: An Introduction,” in Lester M. Salamon (Ed.), The Tools of Government: A Guide to the New Governance (Oxford: Oxford University Press, 2002), 38.

2. This relationship between government and contractor is an extension of ministerial responsibility that Aucoin and Jarvis define as vertical accountability within government. See

Peter Aucoin and Mark Jarvis, Accountability in Canadian Governance: Complexity, Confusion and Conundrums (Ottawa: Canada School of Public Service, 2005).

3. For a discussion of the functions of accountability, see Richard Boyle, “Maintaining Voluntary Sector Autonomy While Promoting Public Accountability: Managing Government Funding of Voluntary Organizations.” Working Paper No. 1, Royal Irish Academy Third Sector Research Programme, January 2002; Peter Aucoin and R. Heintzman, “The Dialectics of Accountability for Performance in Public Management Reform,” International Review of Administrative Sciences 66, no. 1 (March 2000), 45–55.

4. For example, the terms and conditions of one of the major grants and contributions program, the Social Development Partnerships Program of Social Development Canada, list as its principle objectives to: advance nationally significant best practices and models of service delivery; strengthen community capacity; and strengthen the capacity of the nonprofit sector to contribute information to government and others. See Social Development Canada (SDC), Evaluation of the Social Development Partnerships Program (Ottawa: SDC, 2003). Available on-line: <http://www11.sdc.gc.ca/en/cs/sp/sdc/edd/reports/2002-002437/page00. shtml>.

5. For a discussion on the new governance paradigm see Salamon, “The New Governance and the Tools of Public Action,” 1–47. See also, Jon Pierre and B. Guy Peters, Governance, Politics and the State (New York: St. Martin’s Press, 2000); Jon Pierre, “Introduction: Understanding Governance,” in Jon Pierre (Ed.), Debating Governance: Authority, Steering and Democracy (Oxford: Oxford University Press, 2000), 1–10; Gerry Stoker, “Governance As Theory: Five Propositions,” International Social Science Journal 50, no. 155 (1998), 17–28; and, William Walters, “Some Critical Notes on ‘Governance,’” Studies in Political Economy 73 (Spring/Summer 2004), 27–46.

6. Tom Fitzpatrick, Horizontal Management: Trends in Governance and Accountability (Ottawa: CCMD, 2000).

7. See Steven J. Kelman, “Contracting,” in Lester M. Salamon (Ed.), The Tools of Government: A Guide to the New Governance (Oxford: Oxford University Press, 2002), 282–318. Salamon, “The New Governance and the Tools of Public Action,” 2002, 1–47; Robert Schwartz, “The Contracting Quandary: Managing Local Authority-VNPO Relations,” Local Government Studies, 31, no. 1 (Spring 2005), 69–83. Until New Public Management took hold in the late 1980s, an alternative means to reducing the risk of moral hazard associated with third-party producers was to give preference to nonprofits on the premise that, since they must operate under conditions of constraints on their ability to distribute profits to their owners or members, they were likely to be and be seen publicly to be more trustworthy. It was common practice in a number of human service fields, such as home care and nursing care in Ontario, to give preference to provision by nonprofits. On the theory, see H.B. Hansman, “The Role of Nonprofit Enterprise,” Harvard Law Review 89 (1980), 835–901; Schwartz, “The Contracting Quandary,” 2005, 69–83.

8. John Martin, “Contracting and Accountability,” in Jonathan Boston (Ed.), The State Under Contract (Wellington, NZ: Bridget Williams Books, 1995), 39. Anna Yeatman, “Interpreting Contemporary Contractualism,” in Jonathan Boston (Ed.), The State Under Contract, (Wellington, NZ: Bridget Williams Books, 1995), 127; Barbara Sullivan, “Mapping Contract,” in Glyn Davis, Barbara Sullivan, and Anna Yeatman (Eds.), The New Contractualism? (Sydney: MacMillan Education Australia, 1997), 6. See Osborne and Waterston on the challenges of defining a contract for service provision between government and nonprofits. Stephen Osborne and Piers Waterston, “Defining Contracting,” in Perri 6 and

Jeremy Kendall (Eds.), The Contract Culture in Public Services: Studies from Britain Europe and the USA (Aldershot, UK: Ashgate Publishing, 1997), 17–26.

9. Kelman, “Contracting,” 2002, 282.

10. Sullivan, “Mapping Contract,” 1997, 3.

11. Susan D. Phillips, “How Ottawa Blends: Shifting Government Relations with Interest Groups,” in How Ottawa Spends 1991–92: The Politics of Fragmentation, ed. Frances Abele (Ottawa: Carleton University Press, 1991); Jane Jenson and Susan D. Phillips, “Regime Shift: New Citizenship Practices in Canada,” International Journal of Canadian Studies 14 (Fall 1996), 111–137.

12. Sullivan, “Mapping Contract,” 1997, 3.

13. Julia Unwin, Grantmaking Tango: Issues for Funders (London: Baring Foundation, 2004).

14. Unwin, Grantmaking Tango, 60.

15. Aucoin and Jarvis, Accountability in Canadian Governance, 2005; Mark Considine, “The End of the Line? Accountable Governance in the Age of Networks, Partnerships and Joined up Services,” Governance: An International Journal of Policy, Administration and Institutions 15, no. 1 (2002), 21–40; and, Fitzpatrick, Horizontal Management, 2000.

16. Robert Gregory, “Accountability, Responsibility and Corruption: Managing the ‘Public Production Process,’ in Jonathan Boston (Ed.), The State Under Contract (Wellington, NZ: Bridget Williams Books, 1995), 59–60.

17. Patricia Day and Rudolf Klein, Accountabilities: Five Public Services (London: Tavistock Publications, 1987); National Council for Voluntary Organisations, Accountability and Transparency, (London: NCVO, 2004).

18. See Aucoin and Jarvis, Accountability in Canadian Governance, 2005; Boyle, “Maintaining Voluntary Sector Autonomy while Promoting Public Accountability,” 2002; Marilyn Taylor, “Between Public and Private: Accountability in Voluntary Organisations,” Policy and Politics 24, no. 1 (1996).

19. See D. Leat, Voluntary Organisations and Accountability (London: NCVO, 1986); NCVO,

Accountability and Transparency; and Taylor, “Between Public and Private,” 1996.

20. Gregory, “Accountability, Responsibility and Corruption,” 1995, 60.

21. Aucoin and Heintzman, “The Dialectics of Accountability,” 2000, 45–55.

22. Hierarchies in the public service are rarely this simple, however. Aucoin and Jarvis correctly note ‘complex hierarchies’ are often the norm in public bureaucracies as opposed to the ‘simple hierarchies’ described above. Those federal agencies with the authority to intervene in departmental activity regarding certain aspects of administration (for example, the Public Service Commission intervenes to ensure human resources management activity is effectively executed according to standards) create complex hierarchies in which public servants have multiple accountabilities so the superior-subordinate relationship is transformed somewhat as subordinates have more than one superior to whom they are held accountable. See Aucoin and Jarvis, Accountability in Canadian Governance, 2005; Considine, “The End of the Line?” 2002, 21–40; and Fitzpatrick, Horizontal Management, 2000.

23. Aucoin and Jarvis, Accountability in Canadian Governance, 2005, 31.

24. David A. Good, The Politics of Public Management (Toronto: IPAC, 2003); Sharon

Sutherland, “Biggest Scandal in Canadian History: HRDC Audit Starts Probity War,”

Critical Perspectives on Accounting 14 (2003), 187–224; and Arthur Kroeger, “The

‘Scandal’ at HRDC.” Paper presented to the Canadian Club (Ottawa, 2000).

25. Social Development Canada, Evaluation of the Social Development Partnerships Program, 2003.

26. See Good, The Politics of Public Management, 2003.

27. Christine Ryan and Peter Walsh, “Collaboration of Public Sector Agencies: Reporting and Accountability Challenges,” The International Journal of Public Sector Management 17, no. 7 (2004), 621–631.

28. See M. Edwards, “Participatory Governance into the Future: Roles of the Government and Community Sectors,” Australian Journal of Public Administration 60, no. 3 (2001), 78–88; Considine, “The End of the Line?” 2002; John Martin, “Contracting and Accountability,” in Jonathan Boston (Ed.), The State Under Contract (Wellington, NZ: Bridget Williams Books, 1995).

29. Considine, “The End of the Line?” 2002, 23.

30. Ibid. at 36. The notion of horizontal accountability is also used within governments, as one department to another. We use it in the context of cross-sector relationships. On the former, see Mark Schacter, “When Accountability Fails: A Framework for Diagnosis and Action,” ISUMA 2, no. 2 (Summer 2001), 134–137.

31. Fitzpatrick, Horizontal Management, 2000, 11.

32. Mark Warren, Democracy and Association (New Jersey: Princeton University Press, 2001).

33. Ibid.

34. These 36 interviews were completed between February and July 2002. Seventeen 17 interviews were conducted with nonprofits receiving a contract from the then HRDC; 12 with nonprofits receiving a contract from Canadian Heritage; and 7 with civil servants and leaders in the voluntary sector.

35. See Social Development Canada’s evaluation of the Social Development Partnerships

Program, 2003.

36. Warren, Democracy and Association, 2001.

37. Susan D. Phillips, “The Limits of Horizontal Governance: Voluntary Sector—Government

Collaboration in Canada.” Society and Economy 26, no. 2–3 (2004), 383–405.

38. Warren, Democracy and Association, 2001.

39. For a discussion of the citizenship dimensions associated with governance or the “New Public Service’ as it has also been called, see Robert B. Denhardt and Janet Vinzant Denhardt, “The New Public Service: Serving Rather than Steering,” Public Administration Review 60, no. 6 (Nov/Dec 2000), 549–559; on citizenship, see also Jane Jenson, “Social Citizenship, Governance and Social Policy.” A paper prepared for the Canada-Korea Social Policy Research Co-operation Symposium in Seoul, Korea, November 2003.

40. Jean Christie, Executive Director of the Voluntary Sector Forum, Pre-Budget Consultations to the Standing Committee on Finance in the 38th Parliament, 1st Session, Tuesday, November 2, 2004. Available on-line: <http://www.parl.gc.ca/infocomdoc/38/1/FINA/ Meetings/Evidence/finae v10-e.htm#T1540>.

41. The Wales executive has been exploring the possibility of moving to ten-year funding horizons, although this move appears to be at least temporarily stalled. See the Final Report of the Independent Commission to Review the Voluntary Sector Scheme (March 2004).

Available on-line: <http://www.wales.gov.uk/themesvoluntarysector/content/annualreport/final/cover-note-e.htm>. In the late 1990s, the PQ Government of Quebec established an enlarged funding pool, SACA, and expanded core funding, including support for advocacy organizations. See Rachel Laforest, Politiques et société, 2004.

42. For a discussion of New Zealand, see Wendy Larner and Tony Mayow, “Strengthening Communities Through Local Partnerships: Building a Collaborative Research Project,” Research Paper No. 2, (Local Partnerships and Governance, University of Auckland, December 2002); Anne Walker, “Overcoming the Neo-Liberal Legacy: The Importance of Trust for Improved Interagency Collaborative Working in New Zealand,” Research Paper No. 11, Local Partnerships and Governance, University of Auckland, April 2004. Australia, see Pat Barrett, Auditor-General of Australia, “Trends in Public Sector Contracting—Some Issues and Better Practices,” Presentation to the Australian Corporate Lawyers Association (March 2001). Available on-line: <http://www.anao.gov.au/WebSite.nsf/Publications/4A256AE90015F69B4A256A22000295FC>; Israel, see Schwartz, “The Contracting

Quandary,” 2005.

43. For the original idea, see I. R. Macneil, “The Many Futures of Contract,” Southern California Law Review 47, no. 3 (1974), 691-816, and on the theory, see James W. Fox Jr., “Relational Contract Theory and Democratic Citizenship,” Case Western Reserve Law Review 54, no. 1 (2003), 1–67. Relational contracting is similar to what DeHoog has termed,

‘cooperative contracting,’ see Ruth H. DeHoog, “Competition, Negotiation or Cooperation –

Three Models for Service Contracting,” Administration and Society 22, no. 3 (1990), 317–340.

44. For a discussion of the parameters, see McKinlay Douglas Ltd., “Government Funding of Voluntary Services in New Zealand: The Contracting Issues,” Available at <http://www. mdl.co.nz/readingroom/governance/govtfunding/framework.html>; Boyle, “Maintaining Voluntary Sector Autonomy while Promoting Public Accountability,” 2002; Schwartz, “The Contracting Quandary,” 2005.

45. See Boyle, “Maintaining Voluntary Sector Autonomy while Promoting Public Accountability,” 2002; 11; also V. P. Goldberg, “Regulation and Administered Contracts,” The Bell Journal of Economics 7, no. 2 (1976), 426–448.

46. Schwartz, “The Contracting Quandary,” 2005.

47. New Zealand’s Strengthening Families Strategy is discussed in Walker, “Overcoming the Neo-Liberal Legacy,” 2004.

48. See Schwartz, “The Contracting Quandary,” 2005.

49. Katherine Scott, Funding Matters: The Impact of Canada’s New Funding Regime on Nonprofit and Voluntary Organizations (Ottawa: Canadian Council on Social Development in collaboration with the Coalition of National Voluntary Organizations, 2003); Canadian Centre for Philanthropy, The Capacity to Serve: A Qualitative Study of the Challenges Facing Canada’s Nonprofit and Voluntary Organizations (Toronto: Canadian Centre for Philanthropy, 2003); Statistics Canada, Community of Caring: Highlights from the National Survey of Nonprofit and Voluntary Organizations (Ottawa: 2004).

50. See Social Development Canada’s evaluation of the Social Development Partnerships

Program, 2003.

51. Voluntary Sector Initiative, Code of Good Practice on Funding (Ottawa: 2002).

52. In England, introduction of a designation of “Compact Plus” for both government departments and voluntary organizations that have agreed to and have demonstrated compliance with the Compact—the agreement between government and the voluntary sector by which each has made commitments as to how it will behave toward and interact with the other—is planned for 2005. It would facilitate passporting in relational contracting on a broad scale, but would do so with a high degree of transparency.

53. In England, for instance, the National Accounting Office (the equivalent of Canada’s Office of the Auditor General) is making a strong case for a more effective performance-based funding regime for contracting that draws on the recognition that funding styles are often confused, and thus serve neither the purposes of the voluntary sector nor those of government particularly well.

54. As Jenson and Phillips note, program officers, particularly those in the decentralized Department of Secretary of State offices, had more engaging and nurturing roles prior to the structural changes introduced in the 1995 budget. See Jenson and Phillips, “Regime Shift,” 1996.

KARINE LEVASSEUR

Ph.D. (cand.), School of Public Policy and Administration, Carleton

University, Ottawa, Ontario

SUSAN D. PHILLIPS

Professor and Director, School of Public Policy and Administration, Carleton University, Ottawa, Ontario