The sector monitor is a new survey program of Imagine Canada that will regularly gather information on the issues facing Canada’s charitable and nonprofit sector. This article presents highlights from the first Sector Monitor, which asked charitable leaders about the impact of the recent economic downturn on their organizations.

The first version of the Sector Monitor surveyed the leaders of registered charities that had annual revenues of $30,000 or more and that were not religious congregations. The survey was conducted online between November 24, 2009, and January 11, 2010. A total of 3,126 leaders were invited to complete the survey and 1,508 (48%) did so. Most respondents (1,224) led operating charities; the balance (284) led foundations. Most foundation leaders (88%) led public foundations. Responses have been weighted by region, sub-sector, and annual revenue to be more representative of Canadian registered charities overall.

Impact Of The Economic Downturn

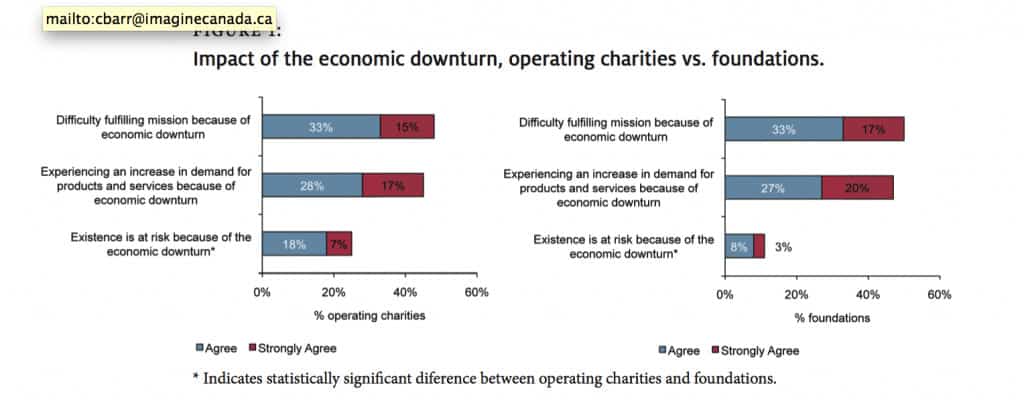

Almost half of sector leaders said they were having difficulty fulfilling their mission (48%) or were experiencing increased demand for their products or services (45%) because of the economic downturn. Almost one quarter (22%) said the downturn had put their organization’s existence at risk.

The leaders of foundations and operating charities were about equally likely to report increased demand and difficulty fulfilling their missions (see Figure 1). However, leaders of operating charities were more likely to say the existence of their organization was at risk (one quarter reported this, compared to one tenth of foundation leaders).

figure 1:

Impact of the economic downturn, operating charities vs. foundations.

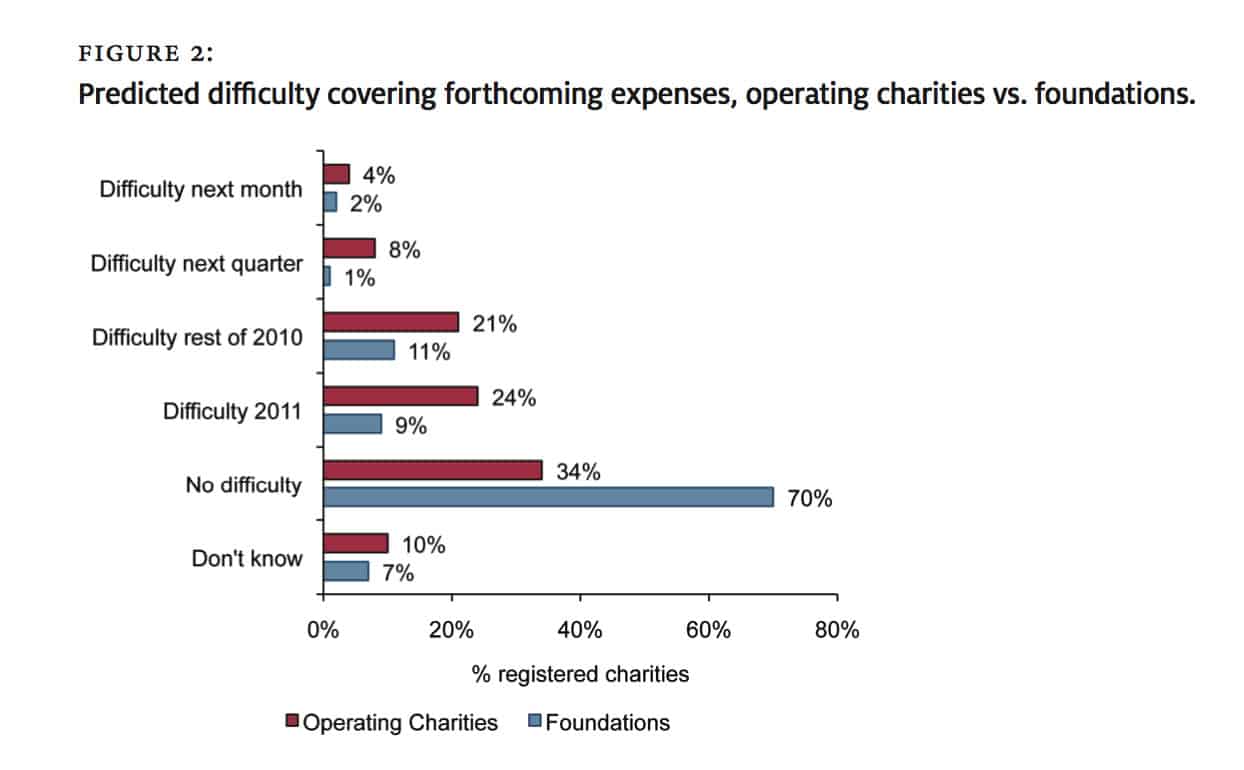

When asked about their organization’s ability to cover expenses over the next two years, 10% of leaders said they would have trouble covering expenses within the next quarter. Just under one fifth (19%) forecast difficulty later in 2010 while 22% saw difficulty coming in 2011.

Operating charities were considerably more likely to predict difficulty covering expenses than were foundations (see Figure 2). Almost one in eight operating charities expected to have difficulty covering expenses within the next quarter, one fifth saw difficulty during the rest of 2010, and one quarter during 2011.

figure 2:

Responses to the downturn

The Sector Monitor asked leaders whether they had taken any of 21 possible actions in response to the economic downturn.1 Perhaps unsurprisingly, organizations were most likely to take minimally disruptive actions such as trying to increase revenues from existing or new sources or reducing overhead. They were much less likely to take more drastic actions such as reducing or eliminating services or programs or suspending grantmaking.

Foundations were less likely than operating charities to engage in most actions (see Table

1). Given their generally small staff complements, it is not surprising that foundations were less likely to take actions relating to human resources. They were, however, also less likely to try to increase their effective financial resources, collaborate with or explore merging with other organizations, and stop accepting new grant requests.

Although charities responded to the economic downturn in several ways, leaders viewed some responses as more important than others. Leaders of operating charities and foundations generally agreed that measures related to increasing effective financial resources were the most important. Beyond financial measures, leaders of operating charities were most likely to cite actions relating to human resources as most important. Foundation leaders were most likely to cite grant-related measures, particularly decreasing the total value of grants made.

Table 1:

Confidence in the future

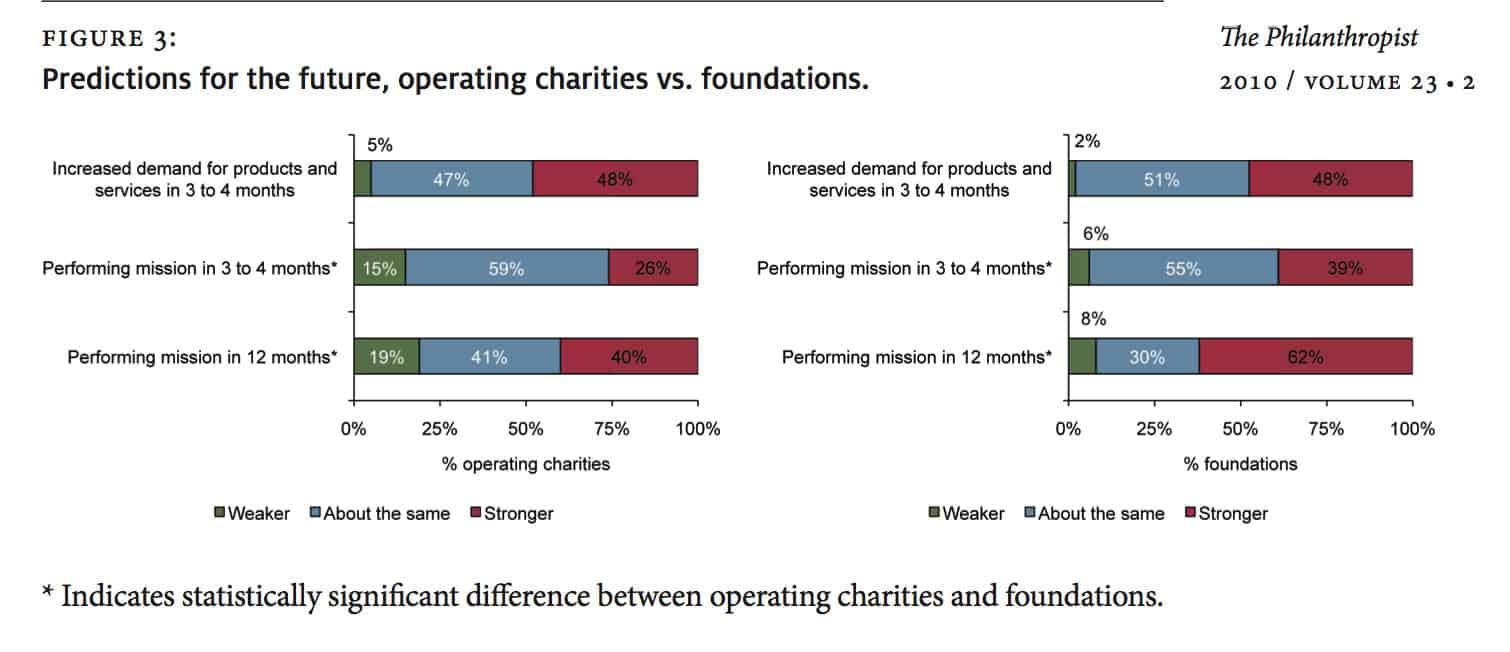

Given the challenges they face, sector leaders are remarkably confident about the future. Almost half (48%) thought demand for their organization’s products and services would be stronger in 3 to 4 months. An equal percentage thought demand would be about the same. In spite of this, more than half of charity leaders (58%) thought their ability to perform their mission would be largely unchanged and more than one quarter (28%) thought they would be in a stronger position in 3 to 4 months.

Foundations and operating charities had similar views regarding demand for their products and services (see Figure 3). However, foundations were significantly more optimistic about their ability to perform their mission in both the short and medium term.

figure 3:

Conclusion

The publication of results from the first Sector Monitor is an important milestone. These results both inform us about the challenges currently facing the sector and provide a baseline for monitoring the ongoing impact of the economic downturn. The value of this survey program will, however, become even more apparent in the years ahead as Imagine Canada continues to collect and publish timely data on the issues and challenges facing Canada’s charitable and nonprofit sector.

Note

1. Only organizations that usually provide grants to other charities were asked the questions pertaining to granting. Only organizations with paid staff were asked most of the questions pertaining to human resources.

David Lasby & Cathy Barr

David Lasbyis a Senior Research Associate and Cathy Barr is Vice President, Operations and Director of Research at Imagine Canada, 2 Carlton Street, Suite 600, Toronto, on m5b 1j3. Email: dlasby@imaginecanada.ca ; cbarr@imaginecanada.ca .