Most individuals have been in a meeting at which an accountant or financial person presents financial information. This can take the form of a budget proposal, a review of the year-end financial statement, or a routine report on operating results at a board of directors’ meeting. Once the presentation begins, the people at the meeting tend to become preoccupied with some other matter as they listen to a presentation that is not engaging and that mentions every item in the financial report even if it is irrelevant. After the information has been presented and it is time for discussion, the conversation tends to fixate on one line in the financial information: the first expense line, whether it is advertising or office expenses. Although a board needs to understand the overall picture presented by the numbers, the natural tendency is to become myopic and focus on a specific detail. It is easier to understand an increase in office expenses than it is to grasp the conclusions that might be drawn from the operating results as a whole. But when the discussion focuses on details, this leaves little or no time to allow for comprehension and discussion of the issues that require the board’s attention. This problem is often compounded by the inability of most accounting software to generate reports that are useful to boards. The purpose of this article is to provide a framework that will allow the treasurer, or any other individual who is responsible for conveying financial information to the board or other users, to compile and present that information in a way that facilitates comprehension and generates discussion. The ultimate goal of the process is to help the board make appropriate decisions.

A fundamental standard underlying the presentation of financial information is relevancy:

If information provided by the accountant is to be useful, then, above all, it must be relevant—it must be associated directly with the decisions it is designed to facilitate.”1

Financial information does not have an existence of its own. It exists to provide the user with the information required to make decisions. This standard of relevancy is reflected in other accounting concepts such as materiality, which considers the threshold at which a user’s decision making process will be impacted.

The concept of relevancy becomes particularly important in a not-for-profit setting since the outcomes of a not-for-profit’s delivery of services can usually not be measured exclusively by financial means. In a business context, the primary measure is the impact or ultimate impact on the bottom line. In a not-for-profit setting, the goal is not to generate a profit and, as a result, most organizations operate ideally on a breakeven basis over the long term. Financial information is just as important in both situations, but in a not-for-profit setting, the financial officer needs to be creative in designing and presenting financial reports to ensure the information is relevant to the board and other users.

Impediments to Comprehension

Before we can consider a framework for the presentation of financial information, there are three hurdles that must be overcome. These relate to underlying issues within the organization and the board. Although these hurdles generally cannot be fully removed, it is important that organizations have a clear understanding of them and attempt to address them.

The first hurdle is the problem associated with the accounting records themselves. Most not-for-profits have considerably more complicated accounting records than those that are found in a business setting. This stems from the need to maintain information for each individual program as well as for funding sources. The resulting fund accounting system multiplies the number of general ledger accounts, often exponentially. It is not unusual for a medium-sized not-for-profit to have 8,000 to 10,000 general ledger accounts; in contrast, a business organization of a similar size may run with less than 500. Most accounting software is designed around a business model that may allow for a couple of departments but not the numerous programs that most not-for-profits require. Although the software may be able to maintain the accounting records, the primary problem is that the reports generated from the software tend to be based on the standard balance sheet and income statement that are used in a for-profit business setting. Most entry-level accounting software packages compound this problem because they do not have the ability to accumulate program data in a meaningful way. As a result, a specialized report usually needs to be generated if the accounting information is to be presented to the board in a useful format.

The second hurdle is the level of financial expertise within the organization and around the board table. Many not-for-profit organizations struggle with limited resources, which often makes it difficult for them to match the compensation levels paid by business entities. Although most staff members should be commended for their level of commitment to their jobs, the board needs to honestly consider the level of financial expertise available to it.

Often, the financial staff is able to process the accounting data but lacks the expertise to properly assess and present financial information in a meaningful way. If this is the case, the board may need to get help from the organization’s auditor or from an external accountant to help bridge the gap between the board’s expectations and the ability of the financial staff to meet them. Generally, the most economical solution is to provide tools and coaching to existing staff.

The board should also evaluate the level of financial expertise around the board table. In many small and medium-sized not-for-profits, board members, while dedicated to the work carried on by the organization, lack the necessary skills to deal with the financial responsibilities of their role. In order for the board to understand and apply the financial information that has been provided, there must be some board members who have the experience and aptitude to interpret the financial results.

The board should also consider the quality of the professional services that are provided to the organization. Many not-for-profits receive professional services on a pro bono or significantly discounted basis. A common complaint is that these services are not completed in a timely fashion and that the needs of the organization are not given the attention that they would have received if the organization had paid for the service. In this situation, the board needs to consider carefully if pro bono or discounted professional services are in the organization’s best interest.

The third hurdle is the value placed on the financial information within the organization. Although this is linked to the level of financial expertise within the organization, it is a more subjective assessment of the role finance plays and the contribution it makes to decision making. In other words, is finance viewed as a necessary evil or an equal partner with the other functional areas of the organization? Generally, most not-for-profit organizations have management staff and board members who come from the service delivery side of the organization. Since this involves providing value, whether the organization runs a soup kitchen or young offender facility, anyone who is seen as putting the brakes on the provision of these services is viewed as not having a heart or not caring about what truly matters. Although this complaint may be legitimate, financial considerations are a factor in the delivery of services. Most individuals involved with not-for-profits can cite multiple examples of situations where programs were initiated with little or no consideration of the financial ramifications. This can ultimately result in significant harm to the reputation of an organization if it is forced to scale back or close the program.

The perceived value of finance is often reflected in the individuals who rise to the management level within the organization. A manager must not only possess expertise in the delivery of the organization’s services but must also have a working knowledge of human resources, finance, and leadership. If the perceived value of finance within the organization is low, there is a danger that inadequate attention will be given to it and to associated administrative issues. Regrettably, it is quite common for management to have expertise in the area of service delivery but not in finance. Although a not-for-profit organization exists not to earn a profit but to maximize its service delivery objectives, nevertheless these outcomes can be accomplished only with due regard to personnel, finance, and the other administrative components that provide support for those services.

The board should consider the value that it places on finance. Although finance will not generally occupy a significant place in a board meeting, the chair needs to ensure that the financial impact of every decision has been addressed. If this is an underlying problem at the board level, the board must discuss why a firm grasp of finances will help the board make sound decisions.

Financial Reporting Framework

Financial statements prepared under generally accepted accounting principles are designed to comply with the requirements of the incorporating legislation and such other disclosure as is considered appropriate. The foundation for this disclosure is found in the CICA Handbook produced by the Canadian Institute of Chartered Accountants. The statutory financial statements have a significant role to play, and ideally the financial information presented at the board meetings should somewhat reflect the statement of operations contained in these statutory financial statements. However, the statutory statements are designed to present comprehensive disclosure and, as a result, are not always easily understood by a non-accounting person. In order to bridge this gap, this article presents a framework—a high-level working document—that can be used by boards at their regular operational meetings to convey significant operating results and fund balances.

As previously noted, when detailed financial information is presented, most people, including experienced financial personnel, tend to fixate on one or two items. This often leads to significant discussion about those items, leaving little or no time to convey and digest the big picture. This problem is exacerbated when the working document is several pages long since, without clear leadership on the part of the presenter, the normal focus of attention tends to be on details presented on the first page of the document. Often board members will offer comments on specific details that catch their attention. Unless the chair redirects the conversation to issues requiring the board’s attention, the ensuing discussion will often fill the time allotted for financial matters.

It has often been said that if a speaker cannot express the essence of what he has to say in one or two sentences, then he does not have a clear understanding of his topic. In Good to Great, Jim Collins praises the businessperson who has these qualities and whom he describes as a hedgehog. He writes:

To be clear, hedgehogs are not stupid. Quite the contrary. They understand the essence of profound insight is simplicity. … hedgehogs aren’t simpletons; they have the piercing insight that allows them to see through complexity and discern underlying patterns. Hedgehogs see what is essential, and ignore the rest.”2

Although Collins is dealing with management’s modus operandi, the presentation of financial information should operate on the same principle. Although there is a plethora of detail that is conveyed in the financial results, in order to communicate financial information to a board, the presenter must have distilled the detail down to reflect key operating results or underlying patterns and then allow the board to ask for additional detail. If the presentation of financial results starts with detail, there is a danger that the board will never move beyond that to see what the financial information is saying.

Focusing on detail at a board meeting is time-consuming and a non-productive use of the board’s time and resources. In addition, except in the smallest organizations where the board is involved in hands-on delivery of services, the board has delegated the operation of the organization to management. Generally, the operating budget has already provided a framework by which management can make decisions about specific financial transactions. Accordingly, the board needs to operate at a higher level, starting with an overview of the operating results, and should avoid micromanaging the details.

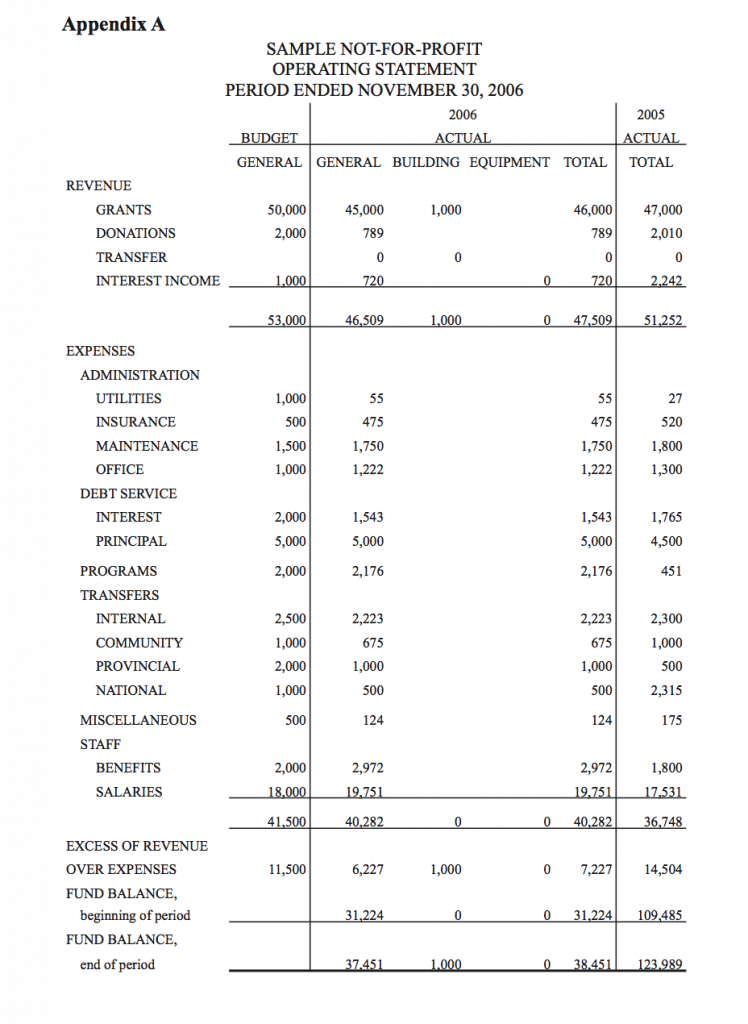

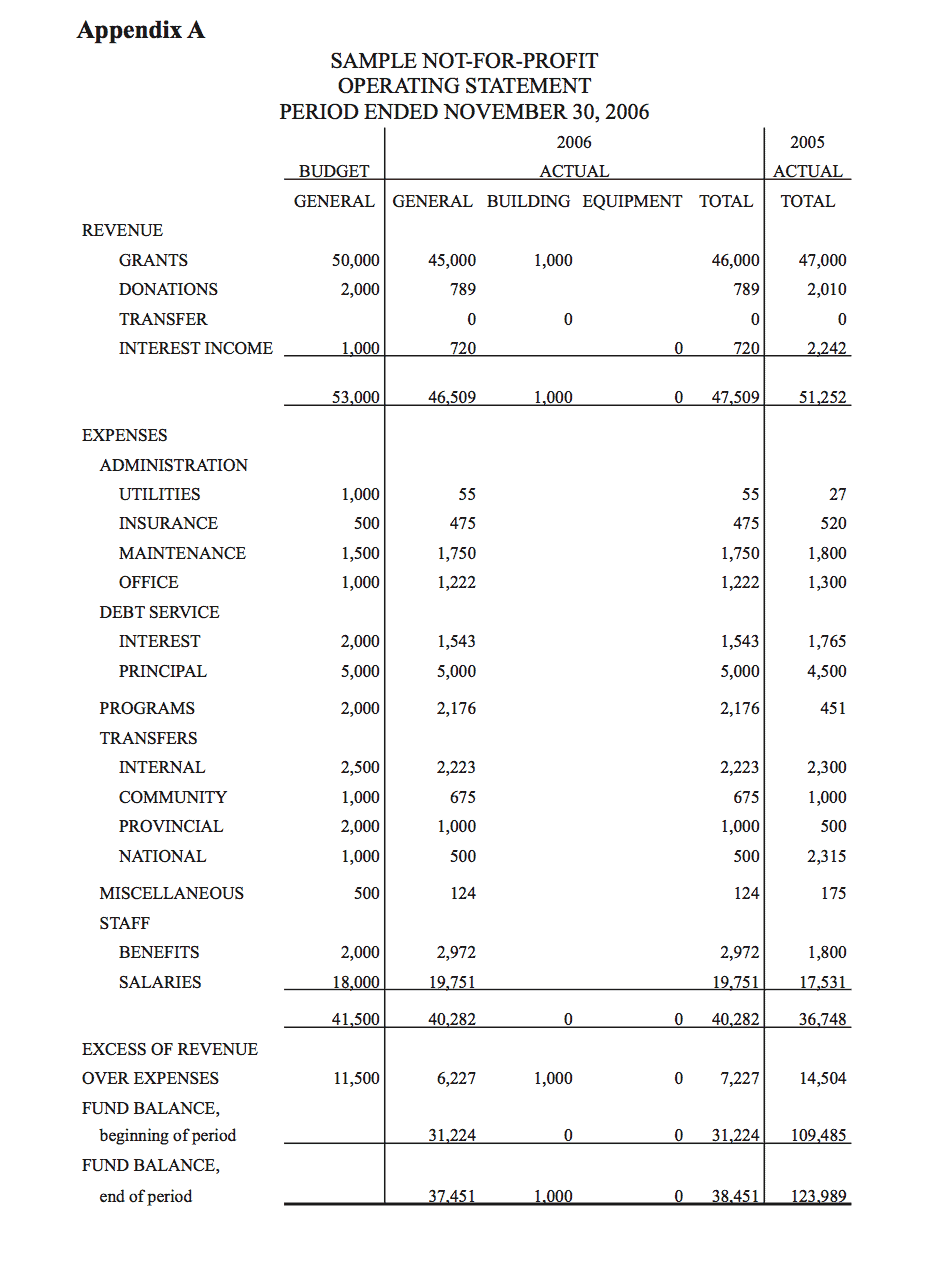

As a general rule, the financial information presented to the board should usually be limited to, or at the very least start with, a one-page summary statement called, for purposes of this article, an operating statement. Although the balance sheet provides a picture of the assets and liabilities of the organization at a specific point in time, the primary focus of the board’s attention should be the operating results for a given period. The operating statement should summarize and present the operating results for the period being discussed and provide information on the equity or resources available for future periods (see Appendix A, page 17, for a sample operating statement).

The objective of the operating statement is to present operating results for the functional areas of the organization, which often revolve around the funds in use by the organization.

Since the objective of the operating statement is to provide an overview, it is important that similar items be grouped together to avoid unnecessary detail. In preparing this summary, the financial officer should review the revenue and expense accounts being used and consolidate the presentation down to a few revenue lines and at most a dozen or so expense lines. In many not-for-profits, in excess of 75% of the operating budget is expended on salaries and benefits. In this situation, there are only a few other expense lines that contain transactions that have a significant impact on operations and that are appropriate for board discussion. For example, in an organization in which salaries and benefits exceed $1 million, it is unproductive for the board to discuss a $500 office expense. The grouping of expenses on the operating statement will help minimize discussions of this nature.

In designing the format of its operating statement, the organization should start with a review of the summarization of revenue and expenses in the statutory statement. As a general rule, the summarization in the operating statement should be the same or similar to the revenue and expense groupings in the statutory statements. This will enhance comprehension as it allows the board to become familiar and comfortable with one method of presentation. This review may also highlight the need to change the presentations and groupings in the statutory statement. Many small and medium-sized not-for-profits simply accept the presentation prepared by external auditors. However, the role of the auditors is to state their opinion on the presentation in the organization’s financial statements. Accordingly, if the organization feels the disclosure can be enhanced in the statutory statement, this should be discussed with the auditors.

When an organization is initially adopting a model for its operating statement, it must generally give the greatest consideration to the columns to be used. The columns should represent the funds or functional areas of the organization. In a small organization, there may only be one or two funds or programs. In this situation, a column would be used for each fund or program. In a larger organization, similar funds or programs will have to be grouped together and presented in one column on the operating statement. For example, an organization that operates several group homes may treat each as a separate fund in the accounting records, but the aggregate operating results of these group homes would be presented in one column on the operating statement.

To determine the columns to be used, it is helpful to start with a consideration of the nature of the funds that exist within the organization. Most organizations maintain their accounting records using the principles of fund accounting:

Fund accounting comprises the collective accounting procedures resulting in a selfbalancing set of accounts for each fund established by legal, contractual or voluntary actions of an organization. Elements of a fund can include assets, liabilities, net assets, revenues and expenses (and gains and losses, where appropriate). Fund accounting involves an accounting segregation, although not necessarily a physical segregation of resources”3

In order to assess the nature of the funds, the financial officer must consider the nature of the restrictions, if any, associated with the funds reflected in the accounting records. As a not-for-profit, the organization and the board have a fiduciary responsibility to the contributor to expend the contributions in accordance with any restrictions imposed by the contributor. Accordingly, it is important that the financial officer clearly understand the nature of the restrictions reflected in the accounting records, which are often distinct from the funds that are used. For example, an organization may run a homeless shelter that is funded from the organization’s own unrestricted resources and a halfway house that is government-funded. In this situation, the accounting records may reflect two different programs, but only the government-funded program has restrictions imposed on the expenditures.

The restrictions associated with funds generally fall into one of three categories:

• donations designated to board-created funds;

• contributions that have been received with an expressed restriction or designation imposed by the contributor; and

• funds transferred internally by a motion of the board.

An organization can operate with board-created funds, such as a scholarship fund. In this situation, where a donation is received to be applied to the scholarship fund, the organization must spend those dollars in accordance with the board motion that created the fund. The organization can also receive contributions consisting of both donations and grants that come with restrictions on how the contributions are to be spent. The organization may not have a specific fund created for these contributions, but a de facto fund will exist and should be reflected in the accounting records. For example, in a religious organization, a donor may give with the expressed intention that the funds be given to another charity. Although a separate fund does not exist for this contribution, the organization should account for this contribution as if it were a separate fund. To further complicate matters, the board can also make a decision to restrict how it will spend certain dollars that are otherwise unrestricted.

An analysis of the nature of the organization’s funds must occur since it is not unusual to find that the accounting records and, occasionally, the statutory financial statements have blurred the distinction between a board-created fund, a restricted or designated donation, and the historical groupings adopted in previous financial statements. In the early years of operation of the not-for-profit, the financial statement presentation is often designed by the external accountant in an attempt to enhance financial statement disclosure. Over time, individuals working with the not-for-profit often assume that this reflects actual board-created funds. Accordingly, before the operations are grouped, it is important that all players understand the interrelation between these restrictions and the presentation within the financial statements. This will involve a review of the funds currently in use in the accounting records. This type of thinking should also occur at the time the statutory financial statements are prepared to ensure that the distinctions are properly reflected.

A common problem associated with donation restrictions is that many organizations have created a separate accounting department for each restricted donation, even if the dollar amount is insignificant. To make matters worse, the accounts created to accommodate these donations may only be used for a one-time occurrence, but the accounts remain in the general ledger for all future periods unless specifically removed. This becomes a particular problem in religious organizations, such as churches, where the members can and routinely do make designated or restricted donations. In this situation, it is often more practical for the financial officer to track these restricted donations in a separate system to avoid creating new departments in the accounting records.

In order to sift through all the funds that may have been created in the accounting records, the financial officer should start by categorizing the various funds into the following categories:

1. funds or departments that exist as a result of a specific motion of the board;

2. departments that exist to allow the not-for-profit to account for restricted or designated donations, which may or may not fall within a board-created fund;

3. funds or departments that exist to comply with a requirement of a funding organization; and

4. funds or departments that exist for ease of accounting.

Often during this process, the organization will find that funds or departments have evolved so that information can be maintained for a specific donation or task. This result is not invalid, but the organization should address, from an operational perspective, which funds should be created by a motion from the board and which board-created funds should be closed. The board-created funds normally represent funds for which the organization receives contributions on a routine basis.

Once the nature of the funds has been determined, the financial officer should consider how to reflect the economic realities of the organization in individual columns on the operating statement. The intention of the operating statement is to reflect the economic units or functional areas that operate within the organization. For example, an organization that operates several group homes that are government-funded and a food bank that is privately funded will require a column on the operating statement for both initiatives as well as a total for the organization as a whole.

Since the operating statement is a working document, it is generally helpful to have a column for the budget as well as a column for comparative figures. The intention of the operating statement is to highlight operating results and focus attention on items that require the board’s attention. Ideally, the budget incorporated in the operating statement will be adjusted for the time period covered. This may also require adjustments to revenue and expenses contained in the budget if they are seasonal in nature. Where the budget and prior period numbers are presented, variances with the current results can be easily highlighted. This generally works well when the organization has one or two key operating programs or economic units, with the balance of funds requiring little or no board attention. When the organization has several economic units, individual budgets for each column on the operating statement would be too complicated. In this situation, only the budget for the organization as a whole should be presented on the operating statement.

In addition to presenting the operating results, it is helpful to present the opening and closing fund balance for each column presented. For many board members, the question will boil down to the working capital of the organization or, in simplest terms, the cash in the bank. Presenting this information on the operating statement allows the board to consider the cumulative impact of its decisions. For example, presenting the fund balance is useful in explaining the rationale for deficits in the current year where the decision was made to expend a portion of the accumulated surpluses from the prior year. The presenter will be able to show the board that there is sufficient surplus from prior periods to cover the deficit realized in the current period.

If further details are to be presented, they should be shown as supplementary schedules rather than attempting to include them in one all-inclusive statement. The intention is to have a one-page document that is easy to comprehend without significant study. A one-page statement that contains too much detail can be as difficult to digest as a document with multiple pages. Accordingly, where the organization has several functional areas that need to be reviewed with the board, a separate operating statement for each unit should be prepared in addition to the one-page summary for the organization as a whole.

The objective of a one-page operating statement is to provide a document that allows the treasurer or other presenter to keep the board focused on the issues that require the board’s attention. Unfortunately, it is not unusual to find that the board has been presented with all the reports generated from the accounting software, leaving the treasurer with the onerous task of navigating the board through them. The presentation of financial information requires forethought and should always start with the summary view.

The summarization of the operating results should be imbedded in the design or account structure of the accounting package. In this situation, the various programs can be grouped together so that the accounting software will produce statements for the economic unit as well as for the organization as a whole. In entry-level accounting software, this type of consolidation is usually not possible. Although the software can produce program statements, the consolidated statement is usually only for the organization as a whole. Although it is beyond the scope of this article, it should be mentioned that financial reporting should be a key consideration in any software upgrade or system conversion implemented by a not-for-profit.

Given the limitations of most accounting software, the operating statement usually has to be generated in a spreadsheet application. This can be performed through manual input of the numbers into the spreadsheet or by exporting the data from the accounting software into the spreadsheet. Once the format of the operating statement has been agreed upon, the preparation of the statement should not be an onerous task. However, it is important to keep in mind that the operating statement is a work in process. The organization will need to adapt it over time to meet the changing needs of the board and the evolving nature of the organization as a whole.

Communication With the Board

Just as critical as the development of a one-page operating statement is the manner in which the operating statement is presented to the board. Ideally, it should be circulated to the board well in advance of the meeting. This will allow board members to review the document and come to the meeting with questions. However, effective communication with the board will only occur if the presenter has a clear understanding of the conclusions that need to be drawn from the financial information.

In order for the presenter to understand the issues that need to be addressed, it is helpful if the following key indicators have been reviewed:

1. Is there a surplus or deficit that needs to be addressed? Generally, an organization will run on a breakeven basis. Where there is a surplus or deficit, the presenter should be able to explain how this will be addressed.

2. Is the surplus or deficit cyclical? For example, donation revenue will often be received in the latter part of the year. Many organizations run with a deficit for most of the year to be offset by donation revenue received in December or government grants received or finalized in March. In this scenario, it is important to consider if the expenses are consistent with the budget for the year.

3. How do the numbers compare with the budget for the period? Is there a significant variance that should be discussed? In making this determination, the presenter will need to consider seasonality to ensure that it has been properly reflected. For example, it is unrealistic for the budget for the month of January to reflect one twelfth of the annual budget on a program that only runs in the summer months.

4. How do the results compare with the comparable period in the prior year?

This should often be the first place to look for reasonableness of the numbers presented. It is important that the presenter is able to explain significant variances between the actual results and the comparable period in the prior year. This will provide an explanation for the changes in operation as well as allow the presenter to address questions raised by other board members.

5. What is the balance of unspent resources? It is critical that the organization always keep in mind the resources that are available to be expended. Accumulated deficits that have been financed by unpaid suppliers are a concern that cannot be ignored even if the organization is operating on a breakeven basis currently.

6. Are there issues within the individual programs that need to be addressed which are not apparent in the group results? This can be in the nature of a deficit in one program that is offset by a surplus in another program.

This list is not exhaustive. Presenters must spend time reviewing the numbers so that they are comfortable with the operating results and have explanations for all significant variances. Generally, these comments should be documented in a memo prior to the meeting. This helps ensure that the discussion stays on track.

When the financial information is presented at the board meeting, the presenter should usually start with comments on the surplus and deficit and on the key indicators, such as donations and salaries and wages. After the overview has been given, the presenter should comment on significant variances and fund balances and direct the board’s attention to areas of concern. In order to put a human face on the numbers, information on the number of people served and the number of employees is usually helpful.

In order to keep the conversation focused, the presenter should normally have a fixed time allotment for the presentation. Where questions are asked that will cause the discussion to focus on irrelevant items, the presenter should address the question by referring to the approved budget or the insignificance of the item. It is not the intention to impede discussion, but rather to ensure that the issues that need to be discussed are presented and properly vetted. It is often helpful for the presenter to consider the dynamics of the board. It is not unusual for the discussion to be dominated by one or two members. In this situation, the presenter may need to solicit the input from members who do not voluntarily provide their comments. Just as non-financial decisions need to consider the impact on finances, financial decisions should only be made after obtaining input from all affected parties.

In the situation where the person presenting the information is being provided with the data from a financial officer of the organization, it is helpful if the financial officer provides a written summary of the facts and conclusions that have been drawn from the financial results. This memo highlighting variances and results should form part of the routine month-end procedures within the organization. In many organizations, this memo will accompany the operating statement.

For this process to work effectively, it is critical that the person presenting the financial information have a comfort level with the numbers. In most organizations, this task is the responsibility of the treasurer. A board must give some thought to who should fill this office. Treasurers do not necessarily need to be accountants, but it is helpful if they have some experience interpreting financial results.

In order to facilitate comprehension at the board level, consideration should be given to the level of understanding that exists around the board table. Most board members join the board with business experience rather than not-for-profit experience. Although most experience is transferable, it is not unusual to find that a board member does not understand the business model of the not-for-profit. Accordingly, without an effort on the part of the board, a new member may operate for several meetings without comprehending the realities of the organization’s situation and, as a result, may be unable to contribute to decision making. In order to address this problem, the board may want to provide an orientation for new members that would include an explanation of the business model and how it is reflected in the financial results.

Summary

The presentation of financial information should not be an onerous task. But it does require forethought. To convey this information, the not-for-profit should consider the use of a high-level one-page operating statement that reflects the operating results for the organization as a whole. In addition, the presenter must have a clear understanding of the financial results to ensure the board’s attention is directed to the areas that need to be addressed. Unlike staff members who work with the issues and financial numbers on a daily basis, the board consists of volunteers who contribute to the organization over and above the commitments they make to their vocation. Given this reality, it is incumbent on the treasurer or other financial officer to convey financial information focused on the issues that need to be addressed in a manner that facilitates comprehension and generates discussion. The operating statement provides a framework for this type of discussion, but it is still just a tool that must be properly handled by the presenter to ensure its effectiveness.

NOTES

1 L. S. Rosen / M. H. Granof, Canadian Financial Accounting Principles and Issues,

(Scarborough: Prentice-Hall, 1980).

2 Jim Collins, Good to Great,(New York: HarperCollins, 2001).

3 The Canadian Institute of Chartered Accountants, CICA Handbook, S. 4400.02(c), April

Appendix A

GORDON P. AHIER

McClurkin Ahier & Company LLP, Waterloo, Ontario

Gordon Ahier is a founding partner in the firm of McClurkin Ahier & Company LLP where a significant focus of his practice deals with registered charities and not-for-profits.