Managers of investment portfolios have a choice of numerous investment styles. A manager’s style could be “top down”, in which case he or she would analyze macroeconomic factors to determine the best investment sectors to be in at any one time. Or, a manager could utilize a “bottom up” investment strategy, emphasizing value in individual investment selection and largely ignoring the big economic picture. Similarly, a manager could be a technical analyst, making investment decisions based purely on securities chart patterns.

Regardless of what strategy managers choose, a great deal of their overall investment return will be determined, not by what individual investments they select according to their preferred investment style, but rather by what asset sectors are emphasized in the manager’s portfolio at any given time. In fact, studies have shown that the most important part of an investment manager’s overall performance is, by far, the asset allocation decision. Specifically, up to 80 per cent of a portfolio’s incremental investment return is derived from the asset allocation mix and only 20 per cent of overall return comes from a manager’s actual securities selection.1 In addition, systematic short-term rebalancing of a portfolio through asset allocation can increase portfolio returns by up to a 1.5 per cent a year as against a buy and hold strategy, without any increase in levels of volatility.2

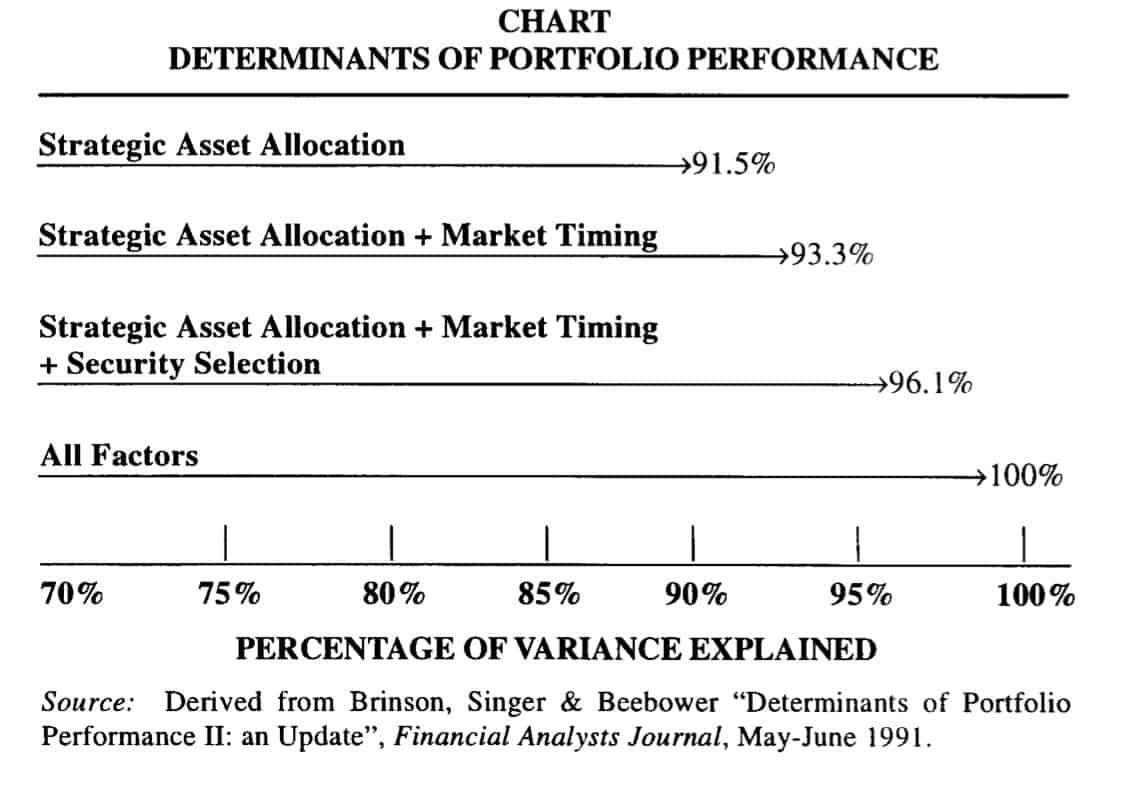

In yet another study which assessed the impact of asset allocation on the total long-term performance results of investment portfolios, it was determined that 91.5 per cent of the returns were attributable to the Strategic Asset Allocation

(See Chart, p.63). As shown in the chart, Market Timing added only 1.8 per cent of incremental value while specific security selection added 2.8 per cent over the preceding strategies.

But what exactly is asset allocation? Simply put, asset allocation determines what percentage of your total portfolio you devote to the numerous asset classes available. It involves an examination of capital markets to gauge future investment returns, combined with an understanding of portfolio objectives, to distribute a portfolio’s assets effectively and efficiently among several asset classes in order to achieve the best return possible within acceptable risk levels. Typically, the asset classes are:

1) Money market instruments (generally called cash)

2) Equity investments (stocks)

3) Fixed-income securities (bonds)

4) Real estate

5) Precious metals or commodities

6) Other assets, depending on the portfolio.

Individual investors will rarely invest in anything other than the first three categories. Investment in the fourth, real estate, is usually confined to purchase of the family home(s). Most institutional investors, on the other hand, will invest primarily in all of the first four categories, with certain hedge funds and other large investors adding “hard assets” categories such as commodities.

Because each of these asset classes will perform differently under various market and economic scenarios (e.g., bonds outperform equities in certain markets, and vice versa), the initial asset allocation mix a manager selects, and how the manager adjusts that asset mix over time depending on capital market conditions, are paramount in determining overall incremental investment performance. Let’s use a very simplified example to stress this point.

Assume we have two managers, A and B, and that both restrict their portfolios to the three main asset classes: cash, stocks and bonds. Now suppose, after examining numerous factors which we will outline below, the two managers decide that their respective portfolios should be “allocated” amongst the available asset classes as follows:

Now suppose that portfolio Manager A is a real wizard at picking high-performing stocks and bonds and manages to outperform his counterpart Manager B in all asset classes over a one-year period, thus earning much higher investment returns than his colleague across all three asset classes. Suppose Manager A also manages to “beat the index” in all classes as well. With this type of performance, we might see one-year total investment returns such as this:

One-Year Total Returns

|

Asset Class |

Index |

Manager A |

ManagerB |

Avs. B |

|

Cash |

10% |

11% |

9% |

+2% |

|

Bonds |

6% |

8% |

4% |

+4% |

|

Stocks |

25% |

30% |

20% |

+10% |

Examining the above table, Manager A, on a performance basis by asset class alone, has clearly managed his individual securities selections better than Manager B. His stock selections have returned 30 per cent compared with B’s 20 per cent, his bond selections have returned eight per cent-twice as much as Manager B-and even his cash component has somehow outperformed B’s. Manager A has also handily outperformed the market indices in the three categories.

Manager A truly looks like a star. But how could a real investment portfolio have performed under these conditions, based on the managers’ initial decisions about asset allocation? Let’s look at a $1000 initial portfolio, and apply both managers’ asset allocations and one-year investment performances. Each manager would have allocated $1000, based on the initial asset allocation decisions, as follows:

|

Asset Class |

Manager A |

ManagerB |

|

Cash |

$50 |

$50 |

|

Bonds |

$700 |

$250 |

|

Stocks |

$250 |

$700 |

|

TOTAL |

$1,000 |

$1,000 |

Now, with these asset mix allocations, let’s look at the Total Return on a $1000 portfolio:

|

Asset Class |

Manager A |

ManagerB |

|

Cash |

$5.50 |

$4.50 |

|

Bonds |

$56.00 |

$10.00 |

|

Stocks |

$75.00 |

$140.00 |

|

TOTAL RETURN |

$136.50 |

$154.50 |

|

TOTAL RETURN(%) |

13.65 |

15.45 |

The tables above show that, even though Manager A had a higher return than Manager B in all three asset classes, Manager B’ s asset allocation mix was superior, resulting in a better overall portfolio performance. In other words, by having 70 per cent of this portfolio invested in equities, Manager B ‘s portfolio was better positioned to take advantage of the rise in the stock market that occurred in our example though his individual securities selections didn’t even beat their respective indices. Thus Manager B, by selecting a more appropriate asset allocation mix, proved to be the better manager.

The above is a very simplified example designed to indicate the importance of appropriate asset allocation. Numerous academic studies have reached the same conclusion: the asset mix in your portfolio is far more important in determining investment performance than individual securities selection. It’s not what you select, it’s where you select it from!

So it’s clear that if you can accurately predict which asset class is going to perform well at a particular time, then you should be able to position your portfolio effectively to take advantage of the expected outperformance of that class. But of course, nothing’s that easy. The asset mix decision involves an analysis of all capital markets and is extremely complex. Managers must be fully cognizant of, and able to interpret subjectively, a wide range of data before even coming close to determining expected investment returns and therefore an appropriate asset mix. In addition, the variables used in selecting an asset mix are continually changing and managers must constantly adjust their portfolio mix to keep it poised for expected market movements. What’s more, managers have to keep their asset mix in line with their investors’ objectives and restrictions at all times, despite their views on any particular asset classification.

Agenda for Asset Allocation Decision

I. Examine All Capital Market Conditions

The key to any sound asset allocation decision is determining which asset class is expected to outperform others in the short, medium and long terms and then positioning your portfolio appropriately by shifting more of your assets into the soon-to-be-outperforming asset class at the right time. Simply put, if the stock market is expected to outperform the bond market, you should have more of your portfolio dedicated to stocks. If the stock market is expected to be weak, add more bonds to your portfolio. But how do you go about determining which asset class to emphasize? Here’s some issues a portfolio manager must consider in determining expected returns from various asset classes:

(a) Recent Returns Versus Historical Experience: Investment managers examine all asset classes’ recent investment returns and compare them to how each asset class has performed in the past. If an asset class has performed below its long-term historical average performance for some time, for example, it’s often an indicator that upcoming returns will be better, returning the asset performance to its more normal level. Thus, “as equity returns stray from their normal relationship vis-a-vis fixed income returns, the forces of the capital markets will pull them back into proper alignment”.3 Despite the proven benefits of examining historical returns to predict future performance, it is still very difficult, and can also be a very subjective indicator because there can often be structural changes in the economy that might lead to false assumptions. Real estate as an asset class, for example, has underperformed other assets and its historical average return now for several years, but it remains extremely difficult to estimate future investment returns from real estate. Today, there is very little consensus as to what we can expect from this asset class in the future.

(b) Market Valuations: Investment managers must consider fully how others are valuing the various asset classes. They do this through market prices. When analyzing expected returns from equity markets, for example, managers must look at dividend yields, price-to-book-value multiples, price-to-earnings multiples, price-to-cash-flow multiples, price-to-sales multiples, expected earnings growth rates and so on. With bonds they must examine credit spreads (the differences in the face value of the rates of return available from different investments), and the “real” rate of interest (i.e., stated rate minus inflation rate). The goal here is to determine if an asset class is over—or under-valued, which can provide clues as to future price directions and expected portfolio returns from that asset class.

(c) Business Cycle Outlook: This examination covers a whole range of indicators from expected GDP to future inflation and interest rate movements. Examining monetary and fiscal policy and other economic indicators is also crucial here. Although timing the business cycle in the short term is very difficult, on a long-term basis skilled managers can get a feel for which way they think markets are heading and select an appropriate asset mix to take advantage of business cycle swings. A manager could, for example, shift a greater portion of the portfolio into long bonds just before he expects interest rates to turn lower, which occurs after the peak of the business cycle.

(d) Technical Position of the Market: Investment managers examine shortand long-term technical charts on equity prices, bond yields, inflation and so on, for clues in determining future returns from different asset classes. Technical analysts believe that chart patterns reflect the sum total of all market information and how capital market participants react under different conditions and use this to estimate future performance. For asset allocation decisions, though, it would be rare for a manager to rely exclusively on technical indicators. Rather, the technical position of the market can serve a more useful function in confirming a belief in a fundamental trend.

(e) Significant Exogenous Factors: Factors such as global economic growth, demographics, political shifts and the like can all have a significant impact on expected returns of all asset classes and investment managers must be aware of such factors when forecasting expected returns.

II. Expectation Predictions and Client Objectives

After examining all of the above data and applying their personal best judgment, managers determine what sort of returns can be expected from the various asset classes under current conditions. Suppose, for example, that after a detailed review, a manager expects the various asset classes to provide the following returns over the next year:

|

Asset Class |

Expected Return (%) |

|

Cash |

8 to 10 |

|

Bonds |

7 to 20 |

|

Stocks |

6 to 12 |

After determining this expected asset class performance, the manager then takes the client’s particular circumstances and objectives into account. A thorough examination of the client’s assets, liabilities, age, tax situation and net worth, combined with an assessment of the client’s tolerance of risk, can help determine what percentage of the client’s assets should be allocated to each asset class, matching client objectives to the manager’s capital market expectations. The best way to match expected returns and client objectives is to determine mathematically the “efficient frontier” for the client, using what’s known as “efficient frontier analysis”.4

The efficient frontier for a portfolio is a quantitative analysis tool that graphically represents a set of portfolios that show the maximized expected total return at various levels of portfolio risk. In other words, it shows investment managers the optimum mix of assets, based on their forecasts of asset class returns and how the returns on each asset class combine to determine overall portfolio performance, as risk varies. Using this analysis, a manager can select an asset allocation mix that both maximizes potential returns and exposes the investments to the degree of risk the client will accept.

It works like this: Theoretically, a client with a high degree of tolerance for volatility, for example, should prefer a greater proportion of the assets in stocks, because stocks provide higher returns, albeit with higher volatility, than bonds. But, based on the manager’s expected asset class returns at various levels of volatility and using efficient frontier analysis, there is shown to be a real trade off between the amount of additional expected return that is added with a higher portion of stocks in the portfolio and the amount of additional risk that is incurred from the incremental equities added. At some point, no matter what a client’s risk profile, it is no longer efficient to keep adding a greater proportion of equities to a portfolio, because the incremental risk isn’t efficiently offset by incremental return.

Efficient frontier analysis, therefore, determines the point at which the most effective asset mix allocation is achieved. Efficient frontier analysis works most effectively in determining the mix of stocks and bonds to be combined with cash to form the investor’s final portfolio but it can be used with other asset classes as well.

Despite the benefits of efficient frontier analysis, asset allocation is hardly an exact science. To offset this, when determining asset mixes a range of expected asset class returns is used because the true predictability of capital market returns is extremely limited. In addition, to avoid the risk of not participating in an asset class which might outperform, and to maintain an adequate level of diversification in a balanced portfolio, the manager will typically establish minimum and maximum percentage allocations for each asset class, so all asset classes are represented at all times, regardless of the expected asset class performance or client profile.

Applying efficient frontier analysis for a very conservative client, a manager might determine the following asset mix:

|

Asset Class |

Percentage Allocation |

|

Cash |

10 to 20 |

|

Bonds |

50 to 60 |

|

Stocks |

25 to 40 |

For the conservative client, these asset mix ranges would be maintained under all circumstances, but the investment manager could fine-tune the portfolio to shift a greater proportion of assets into a particular class as market conditions warranted. This way, the manager can maximize portfolio return but keep the portfolio within the client’s acceptable risk limits as determined by the initial analysis.

Diversifying

Diversification is a good thing in asset allocation, but only up to a point. It all depends on the degree of correlation, or similarity, an asset class has with other classes. Real estate is often added as an asset class because it performs much differently than bonds or stocks under most market conditions and hence reduces overall portfolio volatility.

Commodities as an asset class also add effective diversification but their use can be impractical for most portfolios because of higher transaction costs, low liquidity (particularly important for small portfolios), the necessarily large minimum investments involved, and sometimes excessive volatility. Art and collectibles buyers usually face high commissions and insurance costs as well. Usually it’s better for most portfolios to stay with the three main asset classes. Diversification can still be achieved by diversifying within each asset class. For example, in the cash (or equivalent) portion of the portfolio you could select both provincial and federal government T-bills. With bonds, you can vary the duration of your holdings, and mix in some high-quality corporate issues. Within the stock portion of your portfolio, you can balance a diversified mix of conservative, growth, income and speculative stock issues, in different industry sectors and geographical regions. Such asset selections will reduce overall portfolio volatility.

Sophisticated managers, however, take asset allocation to the next level, and use a variety of higher-level asset mixes and shifting techniques. Some of these include:

Tactical Asset Allocation: Although all asset allocation strategies, by definition, involve regularly readjusting the asset mix of a portfolio, tactical asset allocation is an active portfolio management strategy that seeks to improve portfolio value by utilizing short-term asset class weightings that differ from the long-run asset mix. Managers employing this method use regression analysis5 to build equations to predict shorter-term market movements and quickly adjust their portfolios accordingly. Tactical managers thus are likely to make much more rapid, but smaller, asset shifts.

Insured Asset Allocation: This approach is designed to improve the “fit” between long-term portfolio results and an investor’s objectives. It establishes “floor” limits on all asset classes, to ensure that a certain level of wealth is maintained under any and all circumstances. As wealth increases, however, the proportion of “riskier” assets in the portfolio increases accordingly.

Problems with Asset Allocation

Despite its proven effectiveness in enhancing portfolio value, several issues regarding asset allocation are continually being debated:

(a) Transaction Costs: Any time asset shifts are made, double transaction costs are incurred (once to sell as you lower an asset class percentage and once to buy another asset class with the freed-up funds). Transaction costs can add up to more than 150 basis points per annum, even at a relatively low portfolio turnover rate. These transaction costs, of course, can quickly erode portfolio returns, and any asset allocation strategy employed must completely offset these costs, or it’s not worth employing. Transaction costs limit the effectiveness of tactical asset allocation and explain why most portfolio managers will only initiate shifts around rigidly-set asset mix parameters and why some managers will only shift assets when expected asset return changes justify a shift of 10 per cent or more of the whole portfolio. Some pension managers employing asset allocation will use futures contracts to “replicate” equities and bond portfolios, in order to reduce transaction costs significantly. However, futures may not be a viable option for many portfolios.6

(b) Missed Opportunities To Switch Assets: Capital markets move quickly. If managers are too slow in interpreting markets, they can miss out on an opportunity to reposition the portfolio and undermine overall portfolio performance.

(c) Historically Based Or Inappropriately Based Information: Most asset allocation managers use computerized models to determine asset mix models and appropriate times to make asset mix adjustments. But stale data can often lead to false interpretations, causing inappropriate, or ill-timed, asset mix switches. Also, many asset allocation models are based on U.S. data which are not always indicative of the Canadian situation.

(d) Different Notions of “Risk”: This problem is particularly troublesome for investment managers who manage both institutional and private money. Private clients typically consider risk to be the potential for, and magnitude of, a capital loss. Certain institutional investors, on the other hand, might view risk as the probability of achieving an investment return below some “benchmark” return. These disparate views can lead to quite different asset allocation decisions and show the importance of managers understanding the client’s objectives.

(e) Illiquidity in the Canadian Market: Certain asset classes, in particular real estate and small-capitalization stocks, are extremely illiquid in Canada.7 This illiquidity can undermine an asset allocation strategy that might otherwise be effective.

Still, despite these potential drawbacks, every investment manager uses asset allocation, whether through sophisticated technical means, pure experience and instinct, or a combination of both. Since asset allocation is the key determinant in overall investment performance, it should not be taken lightly, either by professional investment managers or by individual investors.

Asset Allocation For Charities

While different charities have different investment requirements, one might generalize at least about foundations. A charitable foundation will probably require a slightly higher mix of income-generating assets to meet its disbursement obligations. It might also be more averse to risk, as its eye is on the longer term. However, this must be balanced against the need for long-term growth for survival, particularly if inflation is high.

It might be helpful to adopt a very rigorous policy on the mix of assets at the outset to avoid having advisory staff, often volunteers, spending a lot of time debating day-to-day fluctuations. Such a policy can deal with extreme variations and can become more flexible with experience.

A well-thought-out initial asset mix can define the charity’s risk exposure fairly clearly, for the comfort of its officers and board. This can make later investment decisions less contentious. Since charities invest for the long term, minor shifts in asset allocation can have a significant impact over time. As a result, charities can benefit from asset allocation techniques without incurring undue risk or undue debate about the day-to-day policies.

FOOTNOTES

1. Bodie, Kane and Marcus, “Principles of Portfolio Management”, Investments,

(Richard D. Irwin: 1989).

2. Beveridge and Bauer, “Tactical Asset Allocation”, Canadian Investment Review,

Summer 1994.

3. Robert Amott, “Asset Allocation and Pension Funds: A Specialist’s Perspective”,

Canadian Investment Review, Fall 1988.

4. This “frontier” is the notional line showing the different allocations of assets in a portfolio that would produce the same degree of risk.

5. “Regression analysis” analyzes the average mathematical relationship between a dependent variable-the core you want to watch-and a set of explanatory variables.

6. “Futures” are binding contracts to take delivery of a specified quantity and quality of a commodity, a basket of stocks or other assets at a fixed price, at a fixed date in the future. They suffer from the same drawbacks as commodities investments and also have high margin requirements making it necessary for the investor to have very liquid assets to cover fluctuations in the value of the contract. This ties up assets which could be invested to maximize returns elsewhere in the portfolio.

7. Canadian investments are often illiquid because the market is small and institutionalized so there may not be ready purchasers when a sale is required.

DAVID P. KEELEY

Phillips, Hager and North Investment Management Ltd., Toronto