Although this paper, based on a speech to a conference of the Canadian Industrial Relations Association on June 6, 1987, decribes the benefits of training and development for business enterprises, Dr. Godkewitsch believes non-profit organizations derive comparable advantages.

Introduction

• Training and Development Managers: do you have to wage an uphill battle every year for training budgets because you can’t demonstrate a financial return?

• Human Resource Managers: Are training and development activities get

ting the knife when budgets are cut?

• Line Managers: Have you been looking for some objective way to back up your gut feeling that training and development really do pay off?

Ifyou are in a position to answer “yes” to any of these questions, or if you’re just concerned about managing people cost-effectively, then this article may well meet some of your needs.

The Problem with Current Estimates of the Value of Corporate Training

Most business organizations that do in-house training or that buy training off the shelves of consulting companies do so because they are convinced that ultimately their profitability will be improved. And that is usually true. Training improves workers’ skills, and probably their motivation, resulting in improved productivity and thus, profitability. But to be certain and to be accurate are seldom easy. How much profitability results from how many dollars invested in training? And what kind of training are we talking about?

One of the key problems facing managers who have the responsibility for developing and training people is the problem of providing a clear demonstration of the financial utility of training, i.e., putting a dollar value on the training function.Clearly, a “gut feeling” that funds put into corporate training will somehow translate into a handsome return is not quite enough. In simple language, the key question is: do we get our money’s worth out of corporate training? Or, as the accountants would have it: is investing in corporate business education adding sufficient value to our human resources asset to make it a priority investment? And in cost-accounting: does capital spent on training have a high return on investment and a short payback period, coupled with high present value?

What is Financial Utility?

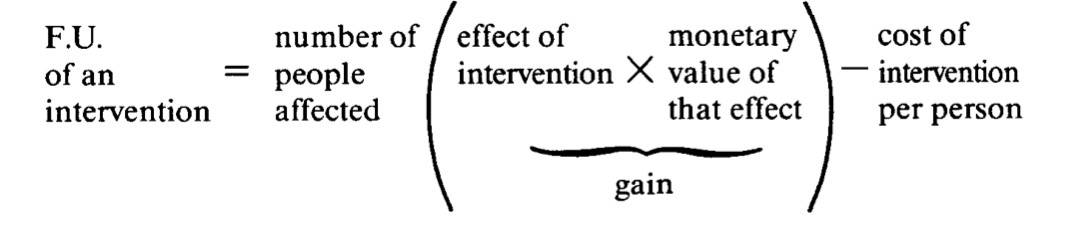

In the last decade quite a few economists, managers and social scientists have sought solutions to problems like these. One general and intuitively simple way to express the financial utility of an intervention (e.g., a training program) is to calculate the gain obtained through the intervention minus its cost. G in can be defined as the product of the effect of the intervention and the monetary value of that effect. More formally the calculation of financial utility will look like this:

If only we could quantify these terms, then we could evaluate any intervention (in this case, training courses) in accounting terms such as direct profit, present value, discounted cash flow, or payback period. While costs and numbers of people affected are usually well known, the other two terms (effect of an intervention and monetary value of the effect) are much harder to pin down. Fortunately recent advances in industrial/organizational psychology now enable us to solve the equation.

Key Problem 1: Quantify the Effect of Corporate Training Any skill, attitude, etc., can be “measured” somehow and will show some distribution of scores. Even fairly unquantified skills such as “overall managerial skills” are measured, when, for example, a group of senior executives must rate that ability in a subordinate group of managers. Normally an evaluation of the distribution of a skill shows a lot of scores at and near the middle and fewer at the extremes. Just as every distribution has a mean, it also has a standard deviation (SD) which describes how “bunched” the distribution is. In a socalled “normal” distribution, about 70 per cent of all scores fall within a distance of one SD from the mean.

To quantify the effect of a training course, we compare the distribution of a given skill among the participants before the training with the distribution of that skill after training. The shift, expressed in SDs, is the effect of that training course. Unfortunately, most organizations do not bother to, or cannot, measure skills before training, much less after, and so do not really know the impact of their training.

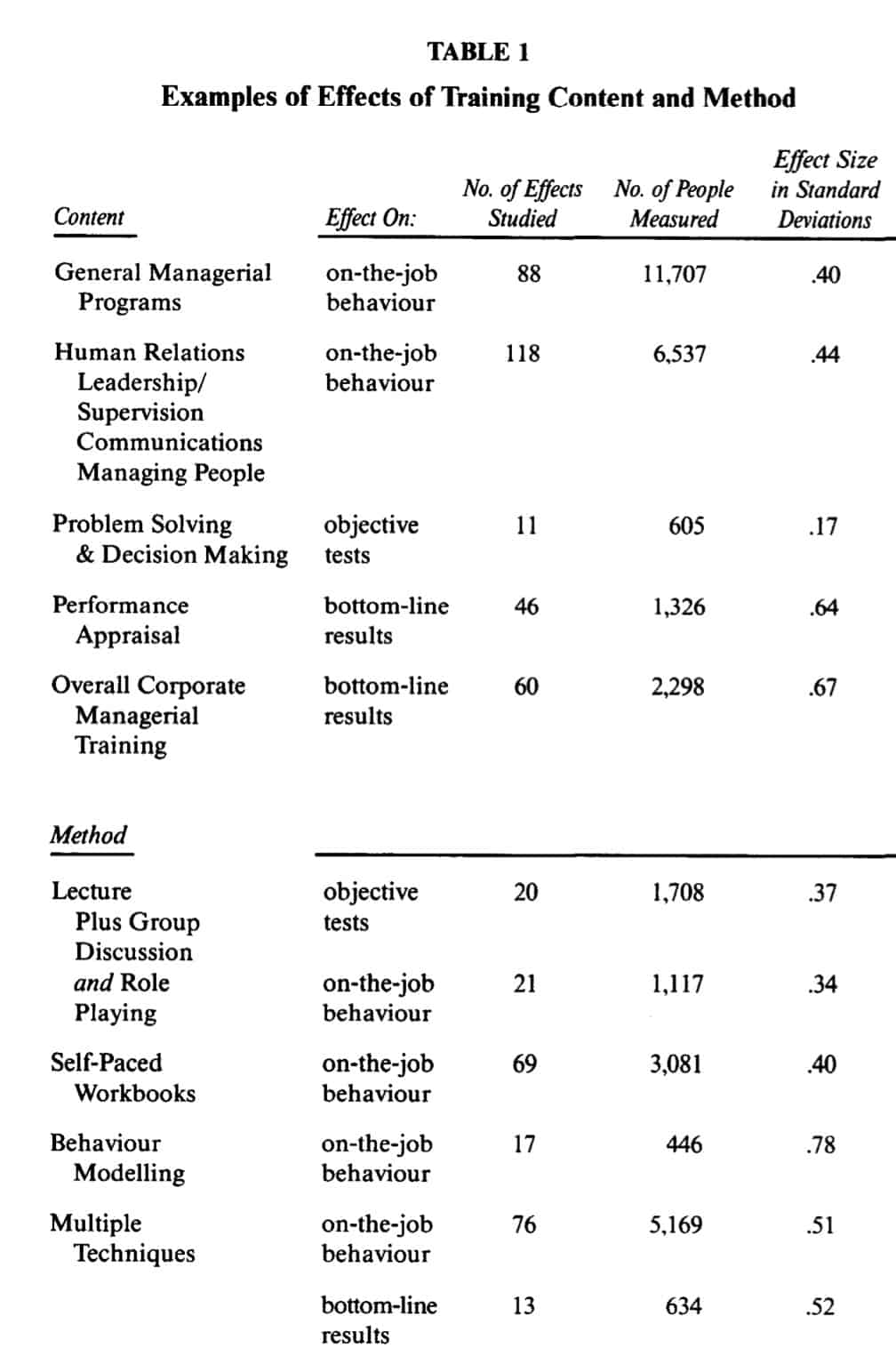

Burke and Day (1986), using a novel technique called meta-analysis, have been able to summarize the findings of70 published and unpublished studies regarding the effectiveness of corporate training. As a result of their work we can now arrive at good estimates of the effects of a range of training programs and training methods using four criteria: subjective learning (judgments of course participants or trainers); objective learning (results on standardized tests); subjective behaviour (changes in on-the-job behaviour as perceived by course participants, peers or supervisors) and objective results (tangible, bottom-line indicators such as reduced cost, improved quality or quantity of output).

TABLE 1 (see image)

Burke and Day provide hard information that summarizes what is currently known about the effects of corporate training in the areas of general management programs (management practice, company policies, etc.); human relations and leadership (including supervision, communications, managing people); self-awareness programs (including sensitivity, laboratory and transactional analysis training); problem-solving and decision-making programs; rater training programs (e.g., performance appraisal); and motivations/values training programs.

Not only do they provide a summary of training effects for each subject area, they also review training effects by teaching method. Knowing the effects of a variety of training methods such as lectures, lectures plus group discussion (with or without role playing or practice), self-paced workbooks, sensitivity methods, behavioural modelling and multiple techniques, is helpful for training managers who are making decisions about training methods at this time of rapidly evolving teaching technology. Table 1 offers some examples of the effects of training content and method summarized from Burke and Day’s work and the first key problem, i.e., how to quantify the effect of training, is at least partially solved. Much more research is needed but what is now known is usable and practical.

Key Problem 2: Quantify the Monetary value of Training Effects on Job Performance

While a training effect can often be quantified objectively, the notion of value is, by definition, tied into what those involved feel and think. Nonetheless in recent years some practical ways have been advanced to express the value of job performance in dollars. Research by industrial psychologists like Cascio (1982), Schmidt and Hunter(1983) and Weekley eta/ (1985) has resulted in the definition of a sensible unit: the standard deviation of job performance. A variety of methods developed to express that measure in dollars fortunately converge to give roughly the same result, i.e.,40 per cent of annual salary. In practical terms this means that for a given job or level of responsibility, a worker who performs one standard deviation below the averagely performing worker (or at the 15th percentile) is seen to be worth40 per cent less than the average salary paid for that job, while the reverse holds for a worker who performs one SD above the average (or at the 85th percentile) who is thus seen to be worth40 per cent more than the average performer. Of course, this does not mean that workers who perform at different levels actually get paid (or even should be paid) such radically different salaries or wages but that political point will not be discussed here.

How to Apply Theory to the Workplace: How Much Are Our Training

Courses Worth?

Quantified expressions for the effects of training and for the value of such effects can easily be applied to actual organizational practice. The findings of Burke and Day can be generalized: the kinds of managerial training and the training techniques they review are from a range of corporations, and therefore any given corporation’s training “menu” is comparable, at least in part, to those reported. This means that any organization can calculate the financial utility of a given training course by “plugging in” the appropriate numbers to the formula we have shown on page 13 even if that organization has not done internal research to assess the effect of its own course. Some assumptions have to be made: that course content, method and culture are comparable between the “norm group” and the one the organization wants to evaluate for financial utility, and that the company’s trainers and trainees are not radically different from the norm group. These assumptions will usually be safe.

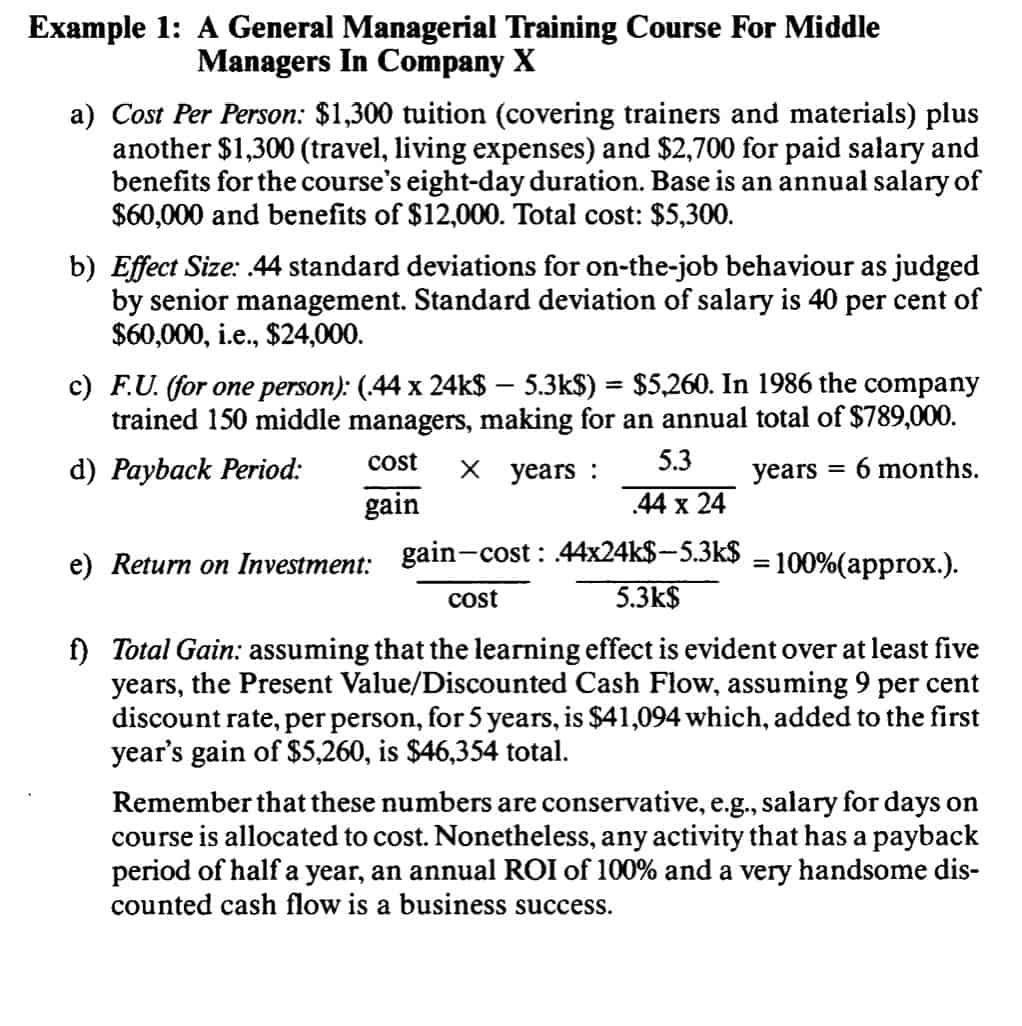

Example 1: A General Managerial Training Course For Middle Managers In Company X (see image)

Example 2: Overall Corporate Business Education in Company X

a) Average Cost Per Person: $3,000 in total, across all courses.

b) Effect Size: .67 on the company’s actual bottom line (i.e., reduced costs, improved output, profitability).

c) Average Salary: 2,500 people were trained in 1986 at an average salary (including benefits) of $62,500.

d) Financial Utility: 2500 ((.67 X .4 X 62.5k$)-3k$] = $34,376,000.

This large sum does not include the discounted cash flow of previous years. Conservatively, this could be another three to five times as great. Although this sounds like an enormous amount of money, it is consistent with the oftenheard statement that employee training and development accounts for a quarter of a company’s profits!

Benefits of Training Volunteers

Since charitable organizations do not pay volunteer staff, they often feel that expenditures on volunteer training cannot be justified. A typical example will refute this conclusion:

• Ten supervisors of volunteers take a Human Resources Management course lasting three days;

• These supervisors spend approximately one quarter of their time at their volunteer jobs so, if paid, they would cost approximately $25,000 plus 20 per cent benefits, or about $30,000 per year;

• The cost of training (including meals and other expenses as well as tuition) is $300 per person;

• Applying the formula on page 14 to this example, we find that the financial benefit (training effect) of upgrading the 10 volunteer supervisors is (see image):

This $10,500 increases to $13,500 if, as is often the case, the volunteers pay for their own training or the course is donated.

In Summary

It is now feasible to report the profits from dollars spent on non-technical training in corporations. Financial accounting can now be applied to business education and to the various teaching methods employed during such training. Training managers, human resource managers and line managers can now give accurate answers to a question that was formerly embarrassingly complex: what is training worth? The described method is proving extremely useful for justifying and validating training budgets wherever it is applied.

REFERENCES

Burke, Michael J., and Day, Russell R. “A Cumulative Study of the Effectiveness ofManagerial Training,” Journal of Applied Psychology,1986, Vol. 71, No.2, pp. 232-245.

Cascio, Wayne F. Costing Human Resources: The Financial Impact of Behavior in

Organizations. Boston: Kent Publishing Co., 1982.

Schmidt, FrankL., and Hunter, Jack E. “Quantifying the Economic Impact of Psychological Programs on Workforce Productivity,” American Psychologist,

1983, Vol. 38, pp. 473-478.

Weekley, Jeff A.; Blake, Frank; O’Connor, Edward J.; and Peters, Lawrence H. “A Comparison of Three Methods of Estimating the Standard Deviation of Performance in Dollars,” Journal of Applied Psychology, 1985, Vol. 70, pp. 122-126.

Summaire

La Formation en entreprise consideree comme un investissement financier prioritaire

Recemment encore, iletait impossible de mesurer les avantages financiers de la formation en entreprise, et I’evaluation de ces programmes relevait plus de la perception de l’evaluateur que de criteres de mesure pecuniaires: une etude plus approfondie des avantages de ce genre de formation et les progres realises sur le plan theorique permettent desormais d’en evaluer le contenu et le mode d’apprentissage en termes d’investissements. Des cas vecus en entreprise sont cites et montrent la facilite d’application de cette methode pour demontrer le haut degre de rentabilite de la formation en entreprise au moyen d’instruments de mesure comme le rendement du capital investi, la valeur actualisee nette et le delai de recuperation. L’emploi systematique de la terminologie comptable pour mesurer les avantages de domaines aussi flous que le perfectionnement du personnel se revele d’une grande utilite pour le gestionnaire des ressources humaines et les chefs hierarchiques.

MICHAEL GODKEWITSCH

Senior Industrial/Organization Psychologist, Imperial Oil Limited