TABLE OF CONTENTS

METHODOLOGY

ANALYSIS OF REPLIES

PROBLEM AREA REQUIRING

FURTHER RESEARCH

GENERAL CONCLUSIONS AND

RECOMMENDATIONS

METHODOLOGY

When we embarked on this pilot study we were in the following position. We had studied in the area of non-profit and charitable bodies and the legislation affecting them for approximately one year, were fairly knowledgeable in this field, had begun to compile a partial list of names and addresses of such organizations, and had prepared several drafts of a questionnaire for non-profit entities.

For this study, we have done the following:

First we completed a final draft of the questionnaire in light of comments we had received from several informed sources. Next we greatly expanded our list of names and addresses of charitable organizations. At present we have approximately 500 in our list but probably not all of these are charitable and certainly not all are private foundations, those organizations in which we are most interested. By comparison, in the United States there is a published list of over 30,000 private charitable foundations and their addresses. It has been estimated that there exist at least 2,000 private charitable foundations in Canada, so our success at compiling an exhaustive list, as is apparent, is obviously limited. However, to our knowledge, it is the most exhaustive in Canada, but much work and cooperation remains to be done before a complete directory of Canadian foundations can be produced.

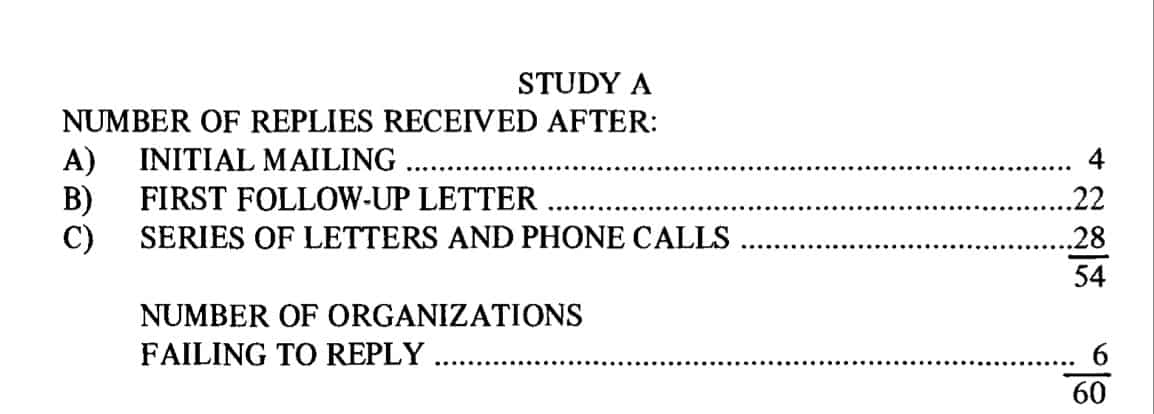

Our next step was to select 60 organizations to approach for our pilot study A. These 60 were selected by no particular criteria except that they are all located in Toronto. These organizations were each sent at the end of May a package containing the following: a letter of introduction from Mr. John Hodgson, Q.C., Vice-President for Ontario of the Canadain Bar Association; an explanatory letter from us; a copy of our questionnaire to be filled in for their particular organization; and a stamped return envelope.

To this initial mailing we received replies from only 4 organizations. Approximately two weeks after the initial mailing we sent a follow-up letter asking for a reply. In response to this letter, we received 22 responses.

Since then we have contacted all the remaining organizations at intervals of about two weeks. In most cases we telephoned personally and usually followed up with a letter, in some cases a personal visit, but in a few instances we could not get through to a responsible person in which case we could only send letters. To this date we have received responses from an additional 28 organizations.

Thus of our original 60 organizations, we have received replies from 54 organizations and no replies from 6.

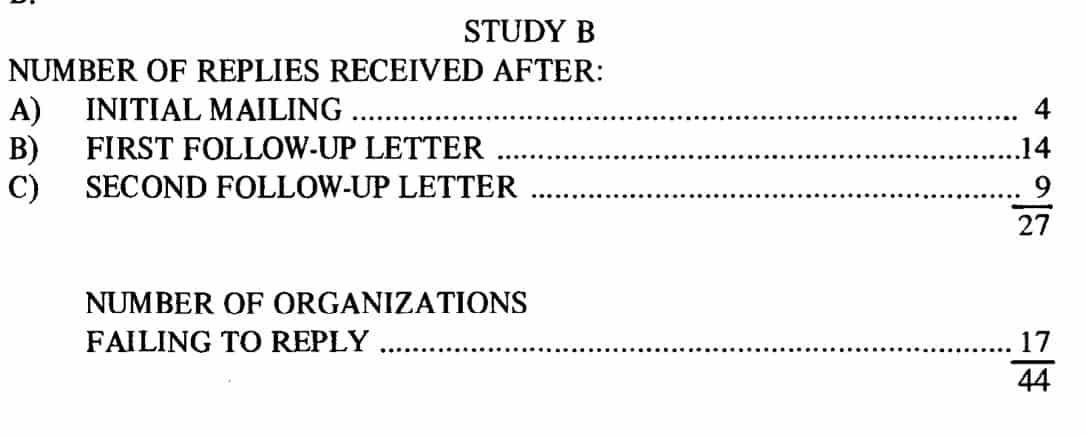

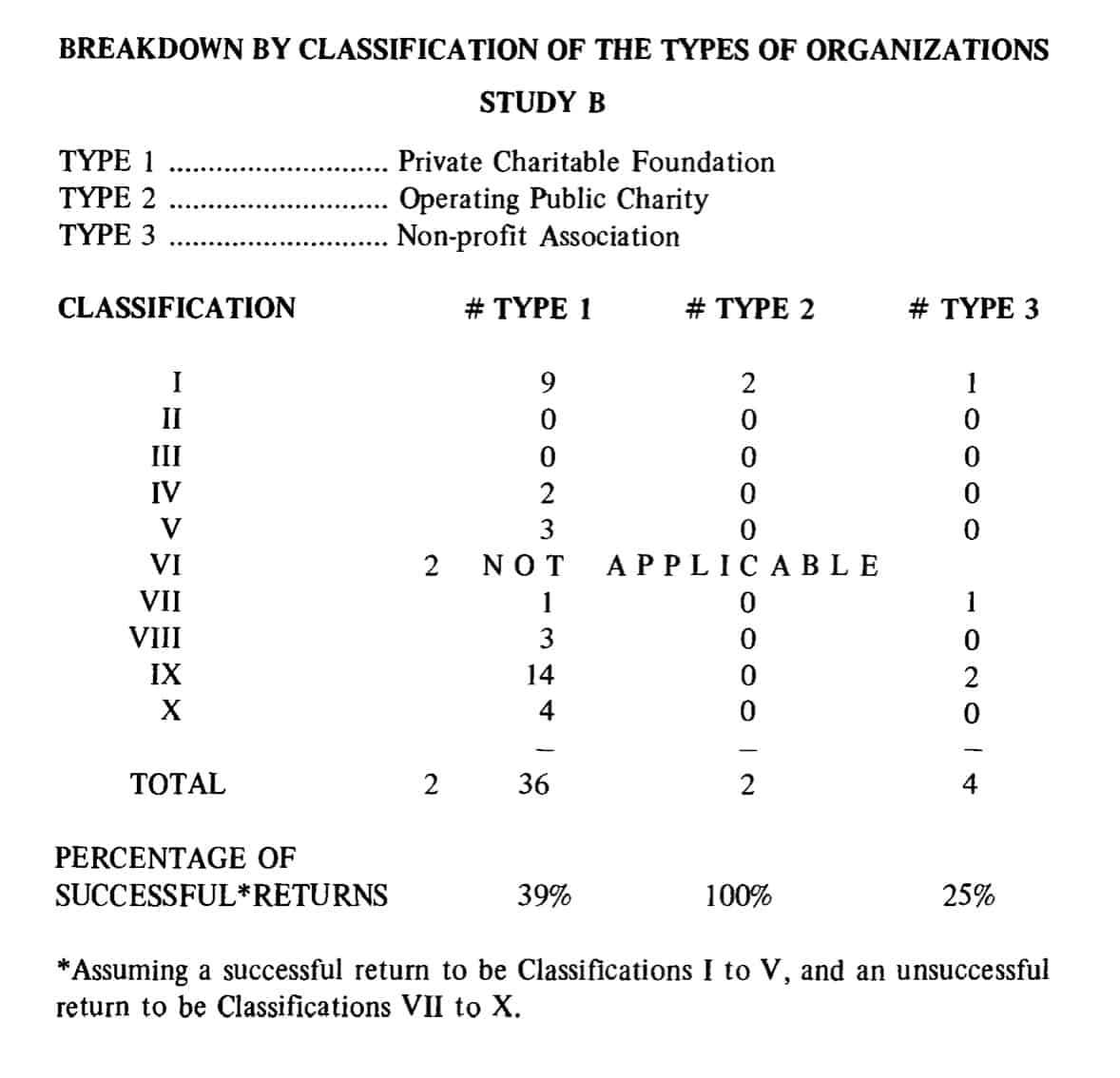

In addition, for comparative purposes, we selected another 44 organizations for our pilot study B. These organizations were mostly from outside of Toronto. They were sent essentially the same package but without the letter from Mr. Hodgson on behalf of the Canadian Bar Association.

To this mailing we received 4 responses.

Again, two weeks later we sent a follow-up letter which brought an additional 14 responses.

At this point, however, we departed from our other procedure and made no further attempt to contact the organizations for about 5 weeks. Then we sent another follow-up letter and to this date have received another 9 responses.

Thus we have received a total of 27 responses from the organizations in study B.

Discussion:

Before trying to assess the success of our pilot study, some comments on our returns must be made.

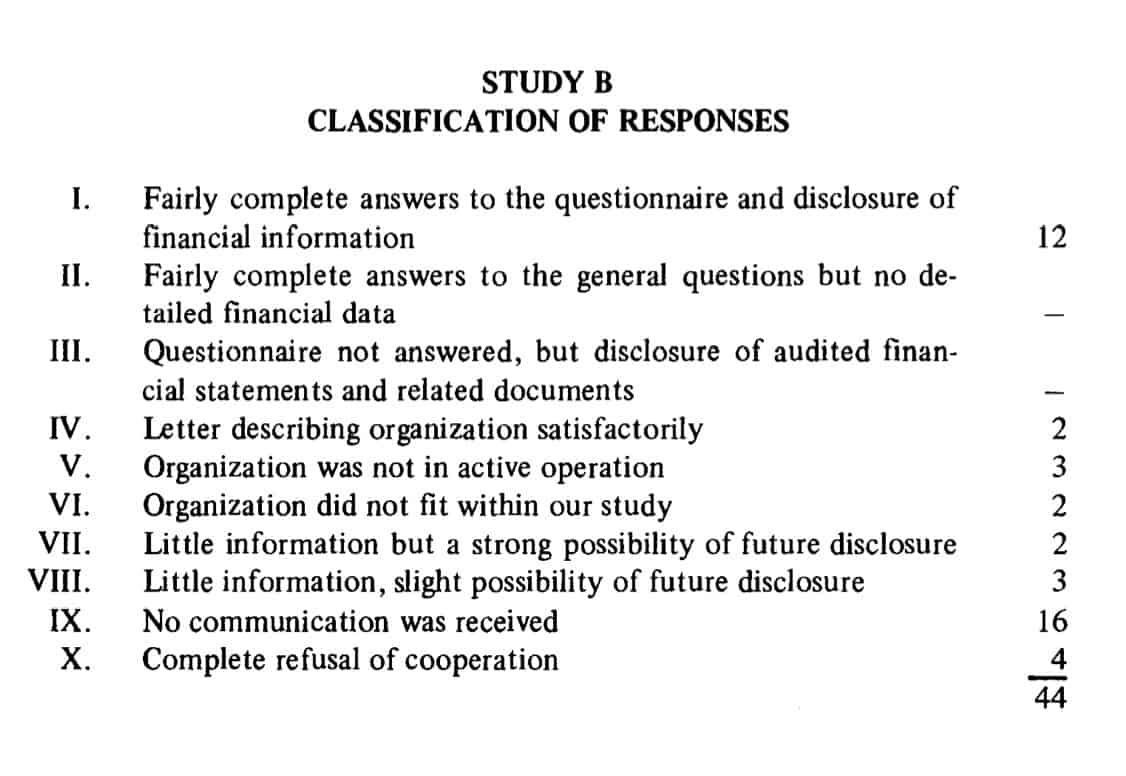

The replies within classification I ranged considerably with respect to their degree of cooperation in our study. On the one hand, there were several organizations which had obviously spent many hours and a great deal of effort in answering our questionnaire and supplying all pertinent information. They were extremely interested in our project, showed encouragement, and several requested copies of our final report if possible. On the other hand, there were organizations which did not necessarily show any great interest in our project but merely granted our request for cooperation. Often they had some apprehensions as to the ultimate use of the information but after clarification responded promptly. However, all the organizations within classification I must be considered as having shown cooperation.

Those organizations in classification II generally showed interest in our project and wished us well, but felt that their financial information was confidential. Nevertheless, we consider these organizations as having cooperated since we told them to feel free to omit information they considered confidential.

The organization in classification III indicated a desire to cooperate but said that the questionnaire was too time-consuming. Therefore it sent us a copy of its constitution and audited financial statements. We consider this to be cooperation.

The organizations in classification IV were usually ones whose operations were very simple and to whom most of our questions had little application. Therefore they merely sent letters describing their organization. Several of these were private conduit-type foundations with no assets of their own. We consider these organizations to have cooperated.

The organizations in classification V are self-explanatory. They had either just been founded and had no significant assets or operations yet, or had been wound up and had disposed of their asset.

the problems of beginning and ending foundations may be obtained from them in the future, this information was not asked for in our questionnaire. Although the cooperation of these organizations was limited, they must be considered to have cooperated as much as they were able.

The organizations in classification VI were either governmental ones or not non-profit. Thus they had no application to our study but cooperated by letting us know.

The organizations in classification VII showed the most diversity. Most of these must be considered to be in the process of cooperating. They have either indicated that they will answer the questionnaire when time permits (some officers are on vacation) or that, although they are not willing to spend the necessary time to answer our questionnaire, have indicated that they would provide specific information on request. In the latter cases, we have interviewed several of the organizations but found it impossible to collect all the detailed information in this way. In other cases, however, we have no real indication that they intend to return the questionnaire, but only that they will consider it. In these cases, usually permission must be obtained from a board of directors or trustees and we must wait until their next meeting. Thus we consider most of the organizations in classification VII as cooperative for now, but some may turn out to be uncooperative in the end.

Those organizations in classification VIII have not outrightedly refused to cooperate but have shown disinterest in our study and a definite disinclination to participation. We would be very surprised if any of these organizations subsequently responds.

The organizations in classification IX have not responded in any way. Despite any of our attempts at communications, we never received a reply from a person of responsibility. It must be assumed that these organizations refuse to cooperate although in a particular case there may be extenuating reasons. In one case, after repeated letters, we received a reply that the responsible person was seriously ill and had been for some time. There may be other situations of this sort, but, in the absence of ev,dence, we can only consider these organizations as completely uncooperative.

Of course, the organi:.ations in classification X must be considered as uncooperative, but some of their reasons for refusing to participate should be noted. Some of them would give no explanation other than “have decided not to supply the information requested”. Despite repeated requests, no further explanations were given. Others replied merely that the information requested was confidential. We thereupon asked them to reply to the non-confidential questions but they refused to do so. It is possible that if we had been able to promise confidentiality, we would have gotten a more favourable reception from one or two of the larger organizations. In some cases, private foundations were apprehensive that the information was going to be used for the purpose of requesting grants, and were hesitant to reply for this reason. Usually after we calmed this apprehension, they replied promptly, but it is possible that others refused to reply because their apprehension was. not completely dispelled. However, in most cases, we can only guess at their reasons for refusing to participate.

Conclusion:

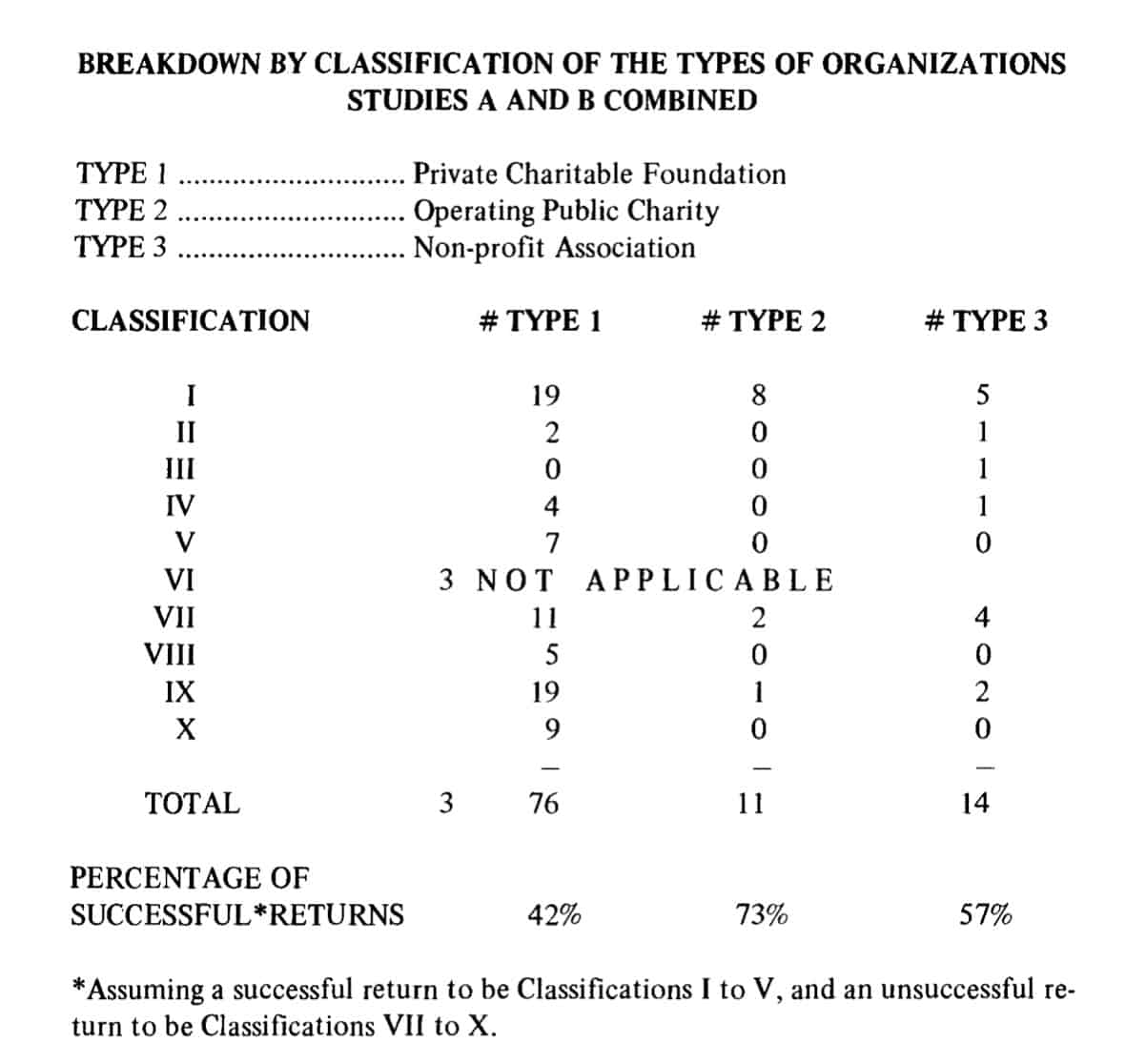

Depending on how satisfactory the replies from classification VII prove to be, the number of organizations we consider to have satisfactorily participated in study A is between 32 and 47. In the end, we are confident that the number will be over 40. This represents a degree of success of over 66% which is far beyond any expectations we had had previously.

On the other hand, the number of organizations on which we have complete detailed information is only 20. But even this represents a 33% degree of success which, in our opinion, is good. However, it must be kept in mind that these figures were attained through virtually 100% follow-up effort in the limited time available.

By contrast, in study B where the follow-up effort was considerably less, the degree of success was about 45%, and the percentage of complete returns was just over 25%. However, the high degree of no responses (almost 40%) appears to indicate that the degree of success could still be raised by more follow-up activity over a longer period of time.

Discussion:

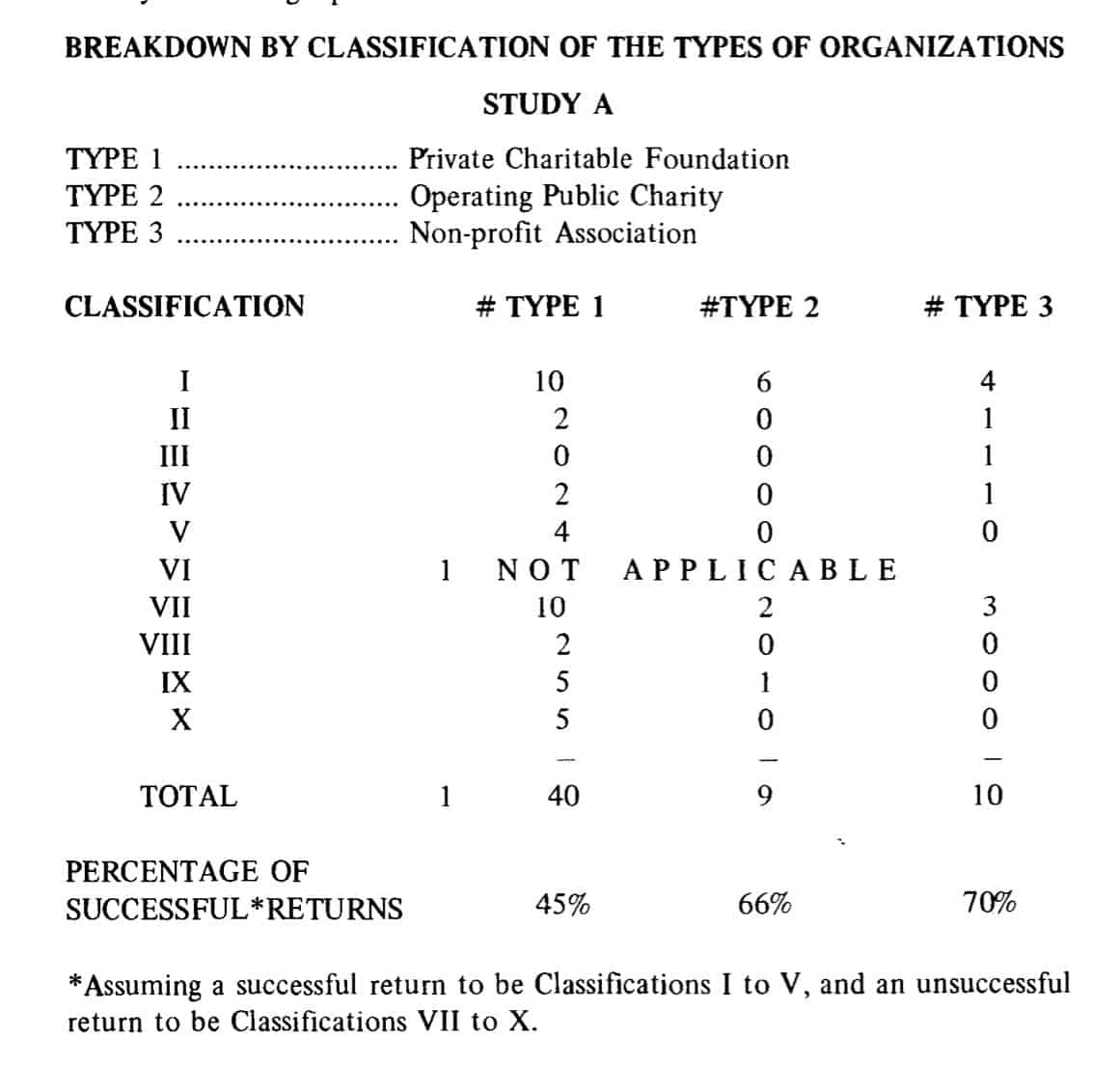

From the preceding charts, it should be noted that although our overall rate of success may be impressive, the rate of success of responses from private foundations ranged only from 39% to 45%, and the rate of classification I responses was about 25%. Nevertheless, this rate of success is still quite respectable.

Conclusion:

Obviously the degree of cooperation of private foundations was appreciably lower than the cooperation shown by operating charities and non-profit associations. This fact ought to be kept in mind in consideration of future projects.

PROBLEM AREAS REQUIRING FUTURE RESEARCH

I. Indefinite Classifications

One of the most basic problems we encountered was trying to classify the organizations we were studying. As a beginning point, we considered all organizations which were tax-exempt by the various subsections of section 62 (1) of the Income Tax Act [s.149 (1) of the Tax Reform Bill]. From these we eliminated the special organizations such as municipal or provincial corporations, certain housing corporations, etc. In the end, we studied only those charitable and non-profit organizations exempt by subsections (e), (f), (g), and (i) [(f), (g), (h), and (1) of the Bill].

The initial difficulty in classifying these latter organizations was deciding which were charitable and which were merely non-profit. Of course, in most cases the distinction was clear, but in many it was not. For example, one of the organizations described itself as a learned society. Basically it existed to further the education of its membership which was open to the public. Although “education” is one of the four heads in the classic definition of charity in Pemsel’s case, the operation of this organization seemed to indicate that it was more like a “society … organized and operated exclusively for … civic improvement”. In its reply to question 22, this organization indicated that it was indeed taxexempt but did not indicate by which sub-section. There were several organizations such as this which we could not classify as charitable or not. In our opinion, a better definition of “charity” is required.

But even amongst those organizations which were clearly charitable, often a distinction between operating charities and merely fund-granting charities was difficult to make. This distinction is a crucial one for tax purposes, much more so

than even a distinction between an operating charity and a mere non-profit organization. In our previous example, whether the learned society was taxexempt through subsection (e) or (i) was really immaterial to its own tax position (although it is material if it wishes to issue tax-deductible receipts for donations). In either case, it could operate virtually unfettered by any conditions imposed on it by the Income Tax Act save only to devote all of its resources to further its purposes.

But in the case of a clearly charitable organization, whether it was tax-exempt by subsection (e) or by subsection (f) or (g) could be extremely significant to its operation because subsections (f) and (g) impose conditions on tax-exemption. Such an organization cannot acquire control of a corporation, cannot carry on a business, cannot incur substantial operating debts, and must expend 90% of its income each year for charitable purposes. An organization exempt by subsection (e) has none of these strings attached to its tax-exemption.

Obviously, an exemption under subsection (e) is preferable for a charitable organization, but in order to be so classified it must be an organization “all the resources of which were devoted to charitable activities carried on by the organization itself.” However, there is no definition of what constitutes a charitable activity carried on by the organization itself. For example, if an organization makes a grant to another charitable body, then this would clearly not be a charitable activity carried on by itself. Equally clearly, if an organization finances a study to be conducted by its own staff, then this would be a charitable activity carried on by itself. However, if that same organization finances the same study by a group of outside individuals, would that constitute a charitable activity carried on by itself? Similarly, does a scholarship granted to an individual constitute a charitable activity carried on by itself? After all, the organization’s activity is merely limited to providing funds, yet it cannot be denied that a charitable activity is being performed.

Note also that even if the organization is tax-exempt by virtue of subsection (f) or (g), the above questions are still important in order to decide whether the organization is fulfilling the requirement of expending 90% of its income for charitable purposes, because, unless those expenditures are considered to be charitable activities carried on by the organization itself, they cannot be counted within the 90%.

Thus, for the purposes of the Income Tax Act, a distinction must be made amongst charitable organizations between those that are wholly operating charities [s.62 (I) (e)], and those that are at least partially fund-granting charities [s.62 (I) (f) or (g)]. We found it hard to make this distinction in many of our cases, and, perhaps even more significantly, we cannot understand the basis for requiring it. We see no reason, for example, why a fund-granting charitable organization is precluded from carrying on a business while an operating charity is not. Furthermore, we do not see the logic in making such a condition a

‘ prerequisite for tax-exemption. Perhaps a better approach would be merely to tax an organization on any business profits without denying it tax-exemption completely. In any case, we believe the distinction between operating charities and fund-granting charities to be hard to make and logically irrelevant. The difficulty of making the distinction was evidenced by the fact that most of the organizations responded that they were indeed tax-exempt but could not indicate under which sub-section.

This conclusion, however, does not mean that we believe no distinctions ought to be made amongst charitable organizations. On the contrary, we favour some sort of classification on the basis of source of funds, whether private, solicited from the public, or through governmental channels. Much more research is required, however, especially in the new U.S. classifications of private foundations, before workable and valid recommendations can be made. However, a new system of classification is urgently required.

One other problem deserving note is the use of the word “Foundation” in a corporate name. One of the organizations we contacted which used that word in its corporate name replied that it was a share-capital business corporation. Perhaps the use of the word “Foundation” ought to be restricted to either non-share capital corporations or to tax-exempt organizations, or both.

II. Use of Foundations to Control Family Corporations

Although we cannot point to an example with certainty where a foundation has been used to retain control of a family corporation, we are fairly confident that this practice exists. For example, one foundation with assets of approximately $180,000 had approximately $170,000 of them in shares of one company. Although this particular organization replied that it did not control or even hold 10% of any class of securities of a corporation, it is evident that potential for abuse exists in some cases and that the present legislation is not adequate to prevent it.

Subsections (f) and (g) deny tax-exemption to a foundation which has acquired control of a corporation after June 1, 1950. However, because of s.62 (3), a foundation is deemed not to have acquired control of another if it has not purchased any of its shares. Because of this, an individual is free to give control of his private family corporation to a foundation set up and controlled by his family. Thus, his family is able to retain control of the corporation without worrying about gift or estate tax problems [or capital gains tax problems in the case of the Bill] .

In Ontario, the Charitable Gifts Act purportedly prevents the gifting of more than 10% of a business to a charitable foundation. However, it may be possible to avoid the intent of the Charitable Gifts Act by merely setting up five private foundations, each controlled by a different member of a family. In any case, legislation similar to the Charitable Gifts Act should be in force in all of Canada.

This potential abuse of the private foundation is an extremely complex problem, requiring complex solutions. We have only indicated here some of the scope of this problem, and it is obvious that much more research is required.

III. Relative Benefits to Society

Historically and logically, the basis for granting tax-exemption to charitable bodies is to encourage the utility of private funds and energy for public charitable purposes. This explanation is predicated upon the theory that these charitable works would have to be done by governmental agencies if the private charities do not do them. Accepting this basis then, it appears to us that the logical conclusion must be that tax-exemption ought to be conditional on some objective standard of public benefit. For example, one foundation reported investments of over $30,000,000 but made only 4% as income on these investments. Of this 4%, 90% (as required) was actually expended for charitable purposes. It must be questioned whether this amount of actual public benefit j’Jstifies the tax-exemption granted this organization.

The requirement that 90% of a foundation’s income be expended for charitable purposes is an attempt at making tax-exemption conditional on public benefit, but it is not sufficient in our opinion. For example, in some cases a foundation’s income may be relatively small, but its use is depriving the government of many dollars in otherwise payable estate and gift taxes.

Furthermore, as in the case of the foundation just referred to, it may be that the foundation is just not generating sufficient income compared to its assets to justify tax-exemption.

Similarly, the use of a foundation often significantly delays the benefit to the public, while the tax advantage is acquired immediately. For example, several foundations reported to us that they act only as conduits for the charitable contributions of its members. While in most cases there is no abuse, it is possible for a member to make a contribution and receive the tax deduction immediately, but the benefit may not reach the public for some time. This delay of public benefit is even greater in the case where the foundation is one with a capital fund, and the member’s contribution is an accretion to capital. In this case, the public benefit may be a very small and gradual one, while the member gets an immediate tax deduction as well as any advantages arising from the control of the foundation’s investments.

One possible remedy to these problems is to require foundations to distribute all of their income unless prior approval has been granted to set aside some part for future use. Furthermore, to discourage foundation ownership of assets which produce little or no income, it could be required that the amount distributed be no less than a minimum investment return on its capital fund. (This approach is currently used in the U.S. where the minimum investment return is 6%. Several of the foundations reporting to us would not conform to this requirement.) Again this problem is extremely complex and requires further research.

IV. Self Dealing

This potential abuse once again stems from the basis of public benefit as a reason for tax-exemption. However, when the services provided, although they may be charitable within the definition of Pemsel’s case, actually benefit the members in more than just a philanthropic way, a tax-exemption may not be justified.

For example, in one case a foundation reported a salary for its executive officer of more than half of the foundation’s charitable donations for the year. In such a way, a person with a large income can use a privately controlled foundation as an income-splitting device or as an income-deferring device.

Several foundations reported that they held substantial amounts of real estate which they had purchased. It is possible for an individual to benefit himself by renting real estate from a privately controlled foundation at less than market price. Thus, although the public may be benefitting by whatever rent he does pay, the individual is benefitting even more.

But perhaps the most obvious and yet unrestricted example of such selfdealing occurs simply when a privately controlled foundation makes expenditures which are strictly speaking charitable, but in which they have an interest. For example, many of the foundations reporting to us are controlled by a company which uses the foundation as a conduit for its charitable contributions.

It is possible for these foundations to conduct charitable activities which may incidentally benefit the public, but which primarily are designed to benefit the company. These activities could be to facilitate research and education in the company’s industry or to provide welfare or scholarship assistance to its employees and their families. Certainly these activities involve a benefit to the public, but it must be questioned whether that benefit is sufficient to justify tax-exemption.

In all these cases (and probably in many more) complex rules to prevent unwarranted self-dealing must be set up, and much research is required.

V. Need to Broaden Foundation Management

If it be accepted that public benefit is the justification for tax-exemption of private foundations, then the argument that their management is a question of private concern cannot be accepted. From the replies we have, it is obvious that most private foundations are managed by small, closely-associated, often family groups. If their avowed purpose is to benefit the public, then perhaps they should be forced to expand their management boards to include outsiders. Such a solution may be preferable to sets of stringent rules restricting investment and expenditure policies. Or perhaps, some sort of public agency should be involved in management.

VI. Effective Sanctions and Enforcement

No matter how effective and appropriate rules and legislation may be, they are useless unless they can be properly enforced.

The information available now to the public is extremely sparse. If a foundation is incorporated and you know the jurisdiction and its official name, you can see its corporate returns. These contain only, however, the address of its head office and the names and addresses of its directors. In Ontario, if its accounts have been passed in the Surrogate Court, these are also open to the public for inspection. However, because of the archaic method of accounting required in the Surrogate Court, these files, while useful, are still limited.

As for the documents required to be filed for Income Tax purposes, these are practically useless for enforcement purposes. (Note that these are not available to the public.) All that is required is a statement of the “aims and objectives as well as the structure of the organization” and a “copy of any financial statements … prepared for such purposes as distribution to members … ” . Although in most cases, we are sure that adequate disclosure is made, it is very possible for the financial statements to reveal almost nothing. In fact, some of the financial statements sent to us reveal nothing more than 90% of the foundation’s income was expended for charitable purposes. Presumably, these financial statements were sufficient for Income Tax purposes.

In Ontario, the Charities Accounting Act empowers the Public Trustee to require a charitable organization to pass its accounts in the Surrogate Court. In practice, many organizations pass their accounts every three years. However, many only pass them at longer intervals, and many never pass them at all.

Even amongst those who do pass their accounts, the method of accounting required is extremely expensive and detailed, so much so that its worth is doubtful. Furthermore, it is easy for an organization to be founded, operate for the less than three years, and then wind up without ever having its accounts passed.

The amount of disclosure to be required and to whom are again complex problems dependent on many factors. However, more stringent enforcement must be attained.

VII. Tax-Exemption and Exempt Income

Under our present Income Tax Act, an organization is either exempt entirely on all of its income, irrespective of source, or it is entirely taxable like any other entity. Section 149 (5) of the Bill introduces a tax on the investment income of certain non-profit clubs but this proposal is still far short of the situation in the U.S. where foundations are taxed on unrelated business income and on investment income in some cases.

More research needs to be done on the provisions of U.S. legislation in this area and its workability.

GENERAL CONCLUSIONS AND RECOMMENDATIONS

As a pilot study we feel that our project has been highly successful. We have demonstrated, in our opinion, that a proper empirical canvas of private foundations would require a follow-up campaign of at least five letters or telegrams over a span of time of at least six months, preferably longer, in order to maximize returns. If such a campaign were sponsored by a sufficiently prestigious organization, such as the Canadian Bar Association, a rate of return approaching 50% could be expected with a minimum rate of full disclosure of 25%.

However, at this point, we feel that such a campaign ought not to be initiated. In the first place, in order to make the study statistically meaningful, as large a sampling as possible must be included. Our greatest disappointment has been that we have full and detailed information on only 19 private foundations. We have been able to illustrate potential problem areas with specific examples, but we have refrained from trying to measure the extent of these problems statistically because our base was too small. We have the names and addresses of hardly more than 200 of the estimated 2,000 foundations in Canada (although we have the names of perhaps another 200) and we feel that this base is not large enough to justify a large scale campaign at this time.

However, what we do recommend for the present is to continue the compilation of a more extensive list. The cooperation of the corporate departments of the governments of all the provinces, as well as the Federal one, ought to be sought for the names and addresses of non-share capital corporations. Also the cooperation of the Federal Department of Revenue should be sought for a list of tax-exempt organizations. When a list of at least 1 ,000 organizations has been compiled, a full-scale campaign could again be reconsidered.

In the meantime, we strongly recommend that the Special Committee on Charitable Organizations of the Wills and Trusts Section of the Canadian Bar Association continue to encourage academic research in the areas outlined earlier in this Report. Many of these same problems have been recently considered in the U.S. and some recommendations have been put into effect. These recommendations and new legislation should be examined for their effectiveness and their application to the problems in Canada. Eventually recommendations for legislative reforms in Canada should be made.

Messrs. Peters and Zaid are two graduate students of Osgoode Hall Law School who undertook the pilot study reported on at the request of the Special Committee on Charitable Organizations.